Read the news at the moment and it's hard to feel optimistic. UK youth unemployment has hit 14.7%, the highest in over a decade, with one in seven young people now looking for work. Energy costs are still high, geopolitical risk hasn't gone away, and prices keep going up in ways people notice at the till. Politicians are now openly floating caps on certain food prices.

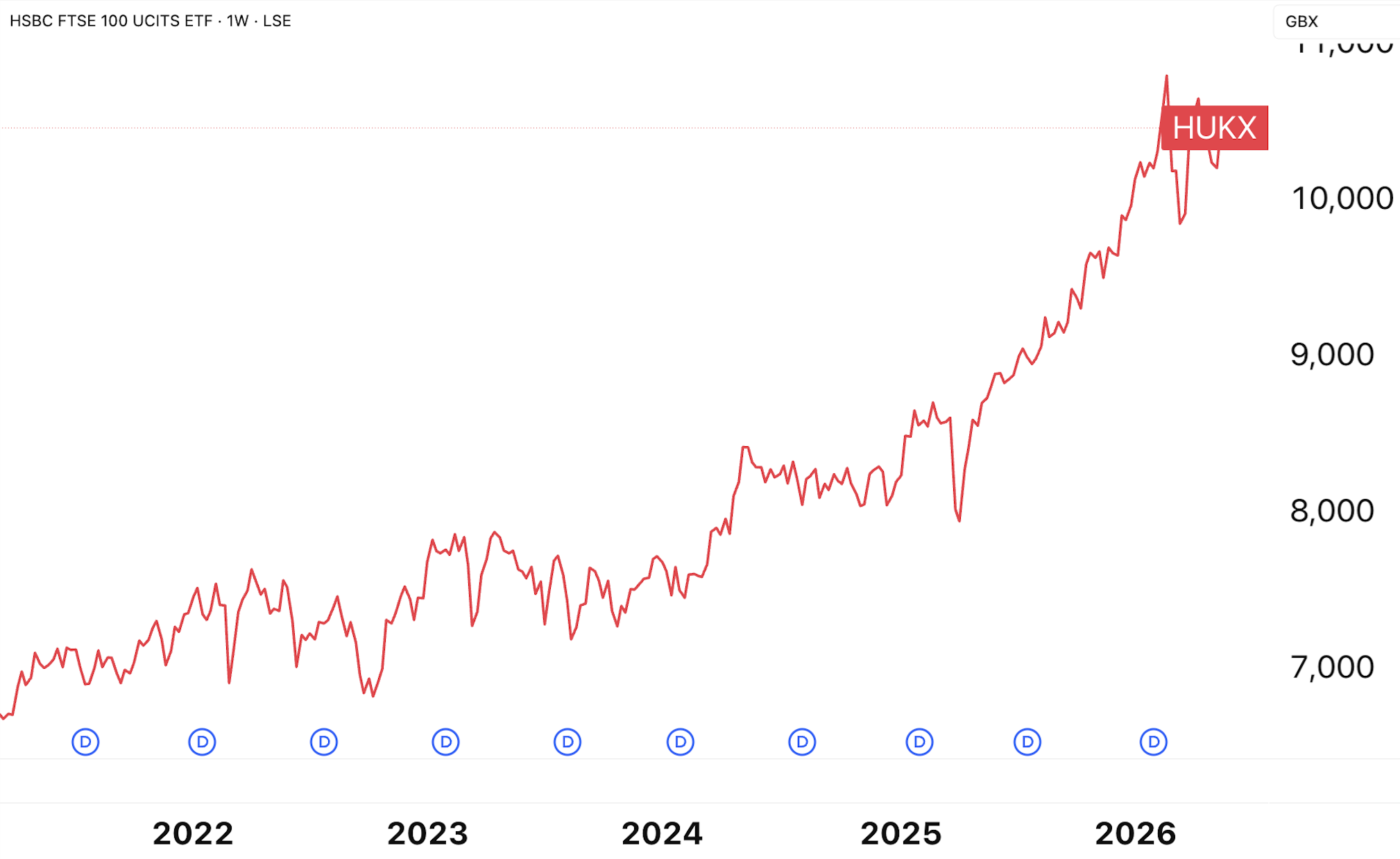

And yet the stock market doesn't seem to care. If you look at corporate earnings, companies are making more money than ever, Nvidia reporting $81bn of revenue for the last 3 months alone and profits are growing fast. Asset prices keep climbing.

The people losing out are the ones holding cash on the sidelines.

Why the disconnect? Most of the analysis points in one direction: AI. Companies adopting it are seeing real productivity gains, and enormous sums are being spent building out the infrastructure behind it. This feels less like a normal cycle and more like a structural shift, comparable to the industrial revolution or the arrival of widespread computing.

Shifts like that always come with the same fear: people losing jobs to machines. Some governments try to slow it down with trade barriers and subsidies, but in a globally connected economy that's a difficult fight to win. Historically, old jobs disappear and new ones take their place. The UK moved from industry to services. Whether it can pull off another transition is the open question, and right now we're seeing the painful side of it as companies trim roles they no longer need.

The honest takeaway is that we don't know how the labour market story ends. What we do know is that the productive side of the economy, the companies driving this shift, is growing fast, and the easiest way to share in that growth is to be invested. Most people aren't. That gap between those participating in the upside and those watching from the sidelines is, in our view, the financial story of this decade.

In this issue:

- Nisba updates

- Halal fund performance (1 month)

- Top savings account

- Fear and greed index

- Platform updates

- Islamic reflection

- Educational focus: Child Trust Funds, the cheapest halal pension, and a story on Caterpillar

- Final reflection

Nisba updates

It's been one of those fortnights where the to-do list keeps growing faster than we can tick things off. But alhamdulillah, that usually means good things are happening including our recent purchasse of an A/C machine. Here's a quick rundown of what's new.

The next Academy cohort starts on June 1st. In just 4 weeks you could have a tailor made financial plan that you will build. A truly one of a kind experience to boost your financial literacy in ways you never imagined. Past attendees have walked away with a completely different relationship with their money, and we'd love for you to experience the same.

Alongside that, our Intro to Halal Investing session is back on the calendar for anyone who wants a softer first step before diving in.

We've also dropped a new YouTube video on pensions and honestly, it's one of the best ones we've done given how much money we are hoping to save you.

New tools

We're paying for a more powerful data source so you can properly compare past performances across funds. Have a play with our new funds page and let us know what else you'd like to see. It's completely free so make the most of it - www.nisba.co.uk/funds

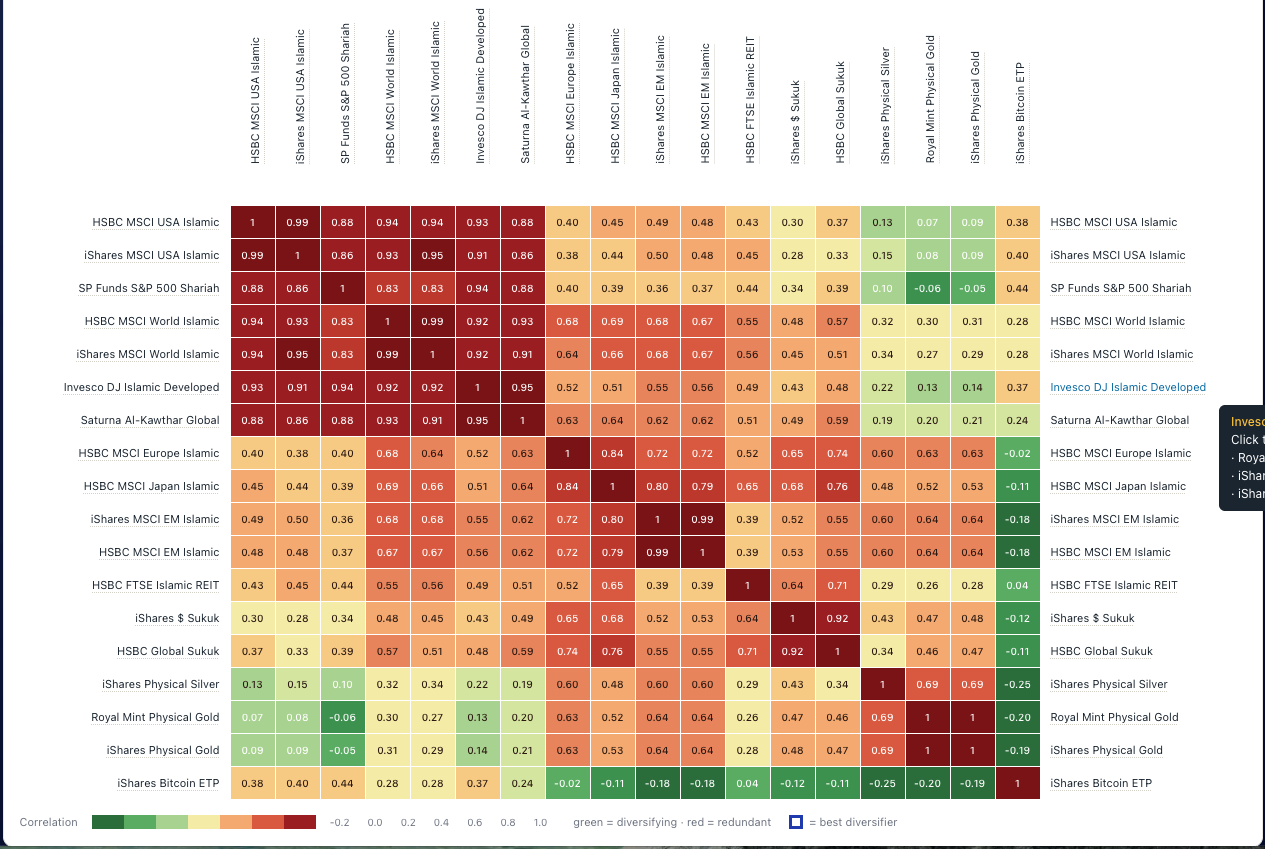

Correlations tool

We keep getting asked which US fund is best, or which EM fund to pick. So we built a page that shows you how correlated two investments actually are, and in doing so, it quietly makes the case that this is probably the wrong question to be asking in the first place.

It might feel a bit overwhelming for most people, but if you've ever had this question, it's worth spending some time with.

Halal Screener

A nice easy way to invest into the stock market and filter out any stocks that don't align with your ethics. Check it out by clicking on the image.

6 steps to halal investing

The Hasan example in particular is such a good way to test your own experience against the framework. If you haven't picked one up yet, it's worth it.

Oh, and Arsenal won the league.

Did you see our push on pensions?

This week Adel made a video about the fees on his workplace pension. Honestly, we are not sure how it has not gone viral, because in two minutes he explained how a 1% saving on fees is going to leave him close to £60,000 better off in retirement, inshAllah.

Sixty thousand pounds. For watching a two minute video, logging into a pension portal, and maybe 30 minutes of work changing provider (providing you know what you are doing).

Too often we see people stressing about how to make an extra £200 or £300 on the side. Picking up extra hours, side hustles, selling things they do not need. All of it costing time and energy they do not really have. And yet sitting quietly in the background is a pension or investment portfolio that, with one small adjustment, could quietly hand them tens of thousands of pounds over a working life. No extra hours. No second job. No exchange of time at all.

This is exactly what the Academy was built around. Not the glamorous stuff. Not the £1,000 a month side hustles. Not the stock that booms 1,000% next quarter. Just the quiet, unglamorous, powerful things that genuinely change the trajectory of a normal person's financial life. The fund choices. The fees. The account types. The employer match. Real solutions for real people, in the right order, explained properly.

One for you to think about this week.

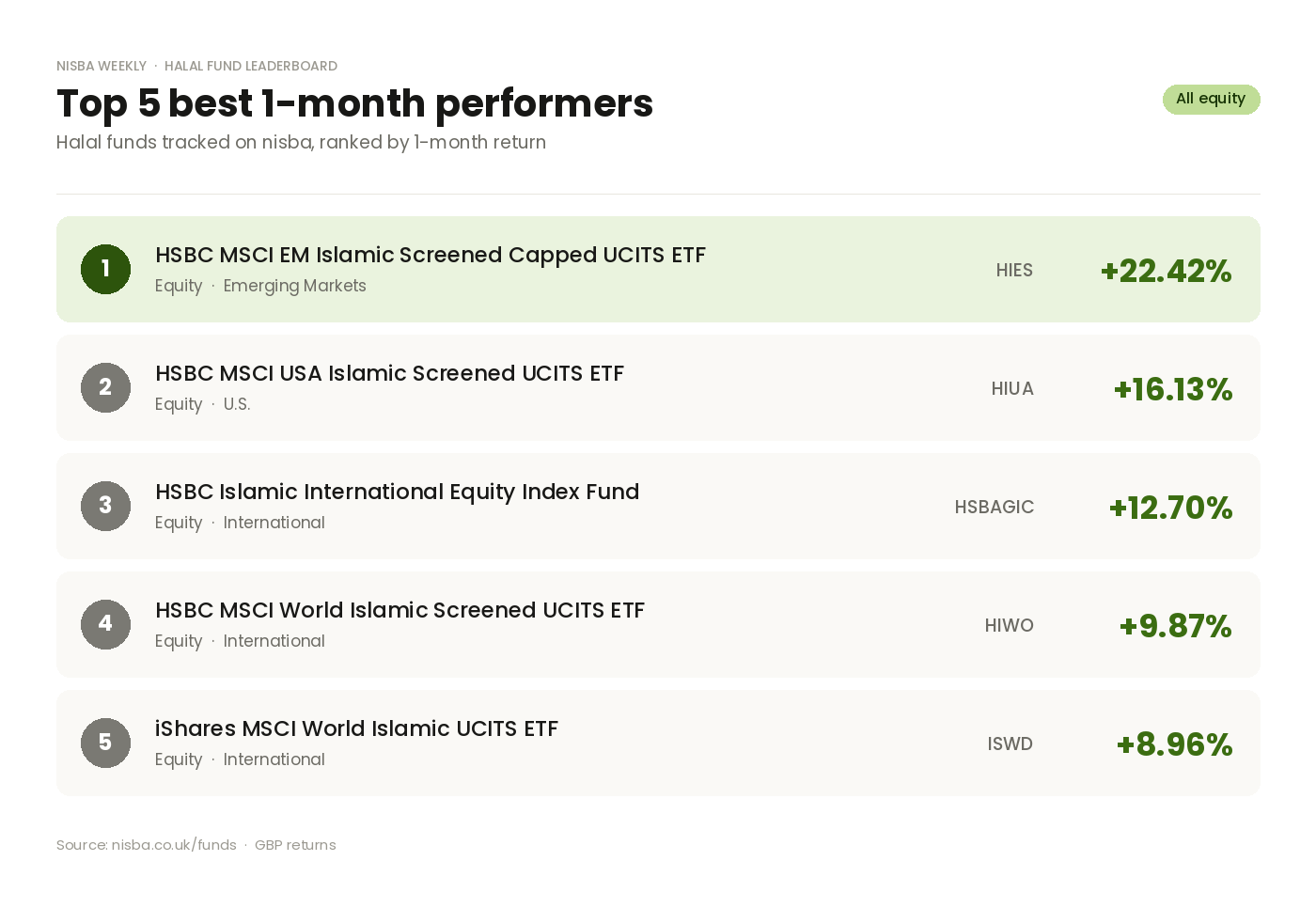

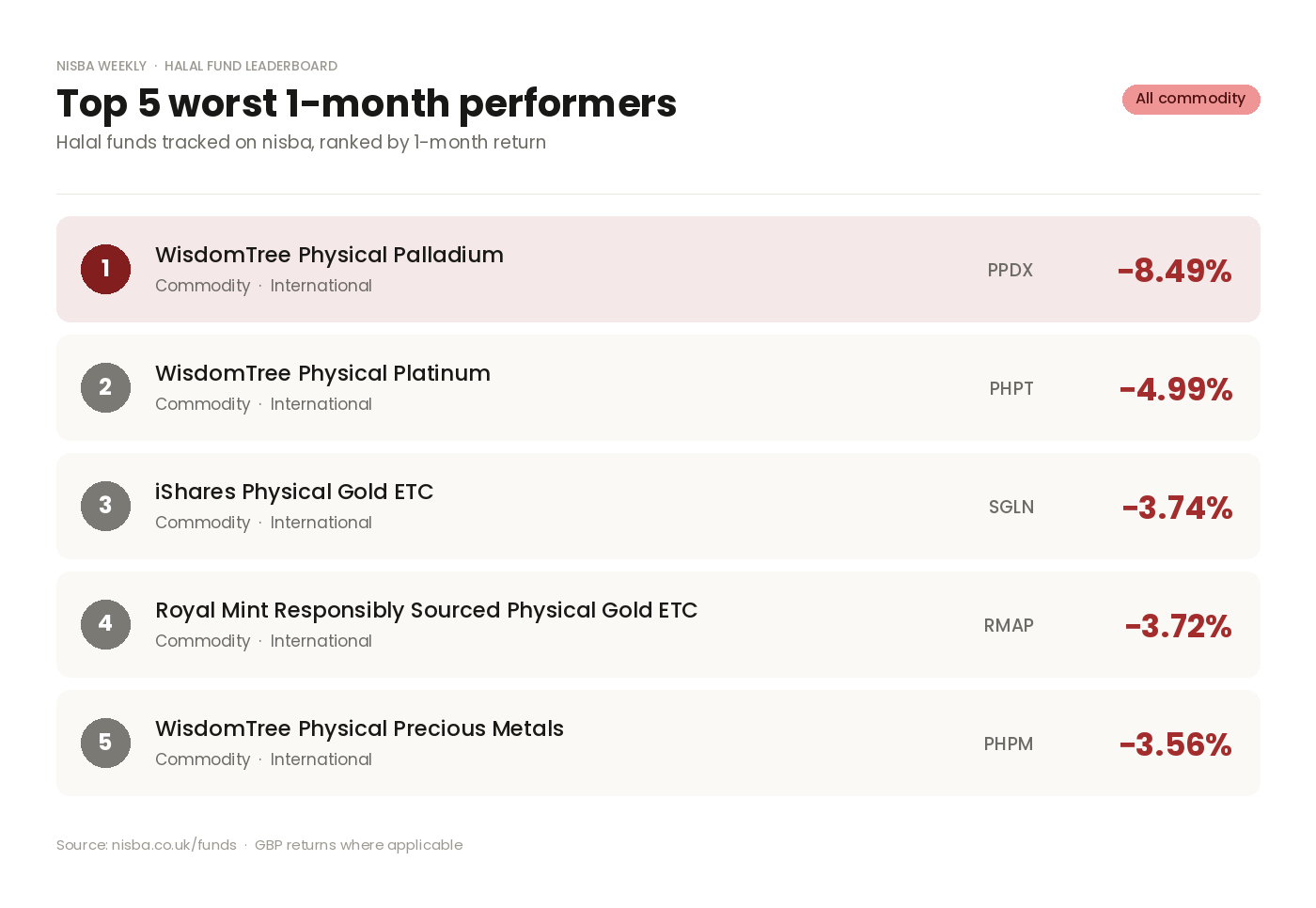

Halal fund performance (1 month)

Big split this month: stocks had a great run while precious metals took a hit. HSBC basically owned the top of the table with four of the five best performers, with emerging markets leading the charge and US and global funds close behind. Meanwhile palladium got hammered, with gold and platinum following it down. A good reminder that the metals rally doesn't go up forever.

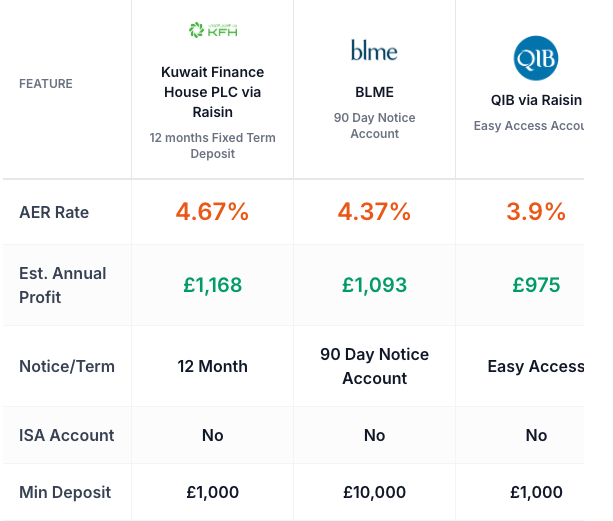

Top savings rate

This week's update on the best Islamic savings rates is a short one. No changes to the top rates for easy access or fixed term accounts, but BLME have improved their 90 day notice account.

As a quick recap of the three types of Islamic savings accounts to consider:

- Easy access - potentially a great place for an emergency fund

- Notice account - worth considering for short term goals

- 12 months fixed term - these can be ideal for a 1 year goal, like going to Hajj in a years time for example

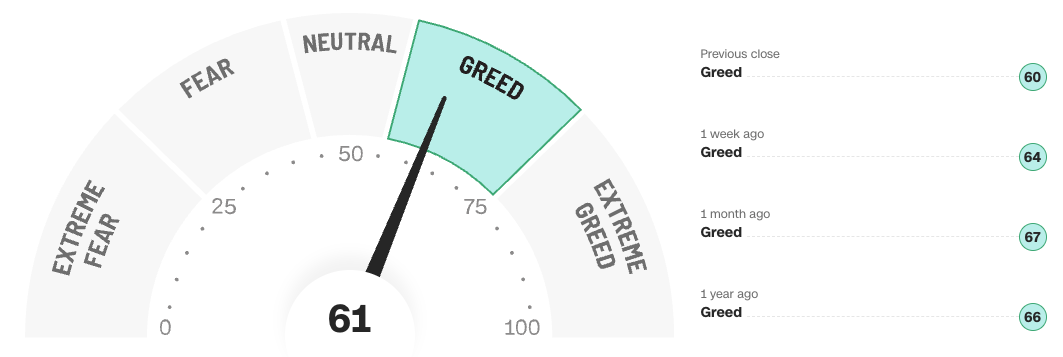

Fear and Greed Index

What is it? The Fear & Greed Index is like a mood tracker for the stock market. It looks at 7 different signals to give the market a score from 0 to 100, where 0 means investors are really scared, and 100 means everyone is feeling super confident and buying everything in sight.

Commentary: Currently the index is sitting at 61 - Greed. The market mood has been remarkably steady, hovering in Greed territory for the past month, with readings of 67 a month ago, 64 last week, and 60 at yesterday's close. A year ago we were in almost exactly the same place at 66, which goes to show that despite all the noise and headlines in between, sentiment can end up right back where it started. For long term investors this is a helpful reminder that the day-to-day mood swings of the market often cancel each other out over time. Staying invested through both the fearful and greedy periods is usually what separates those who build wealth from those who chase it.

Platform updates

Standard Life have released a lifestyling shariah option, a useful addition for anyone wanting their portfolio to de-risk automatically as they approach retirement.

Cur8 Capital have completed a fundraise for a property development.

Pfida have rolled out a new SaveTogether feature, which also shows you how far along the waiting list you are. A small but welcome bit of transparency.

Trading 212 have launched their SIPP. We've applied for ours but it's not live in the account yet, will report back once it is and we've had a proper look around.

Islamic reflection

The 10 Days: A Reminder of why we invest

We're in one of the most blessed periods of the Islamic year. The first ten days of Dhul Hijjah began on Monday 18th May, with the Day of Arafah on Tuesday 26th and Eid al-Adha on Wednesday 27th.

The Prophet ﷺ said: "There are no days on which righteous deeds are more beloved to Allah than these ten days." (Bukhari)

So here's a thought for this week. Open your portfolio less. The market will do what it does whether or not you refresh the page on Tuesday afternoon. Use that energy on things that actually compound in the next life: fast a day, give some sadaqah, make dhikr, call a relative.

And while you're stepping back, ask the bigger question that gets buried under the noise: why are you investing in the first place?

For most of us, the honest answer isn't "to maximise returns." It's to provide for our families without compromising our deen, to be generous, to leave something behind, to have options in old age.

The portfolio is the tool. The niyyah is the point. These ten days are a good time to reconnect the two.

May Allah accept from us all, and grant us a blessed Eid.

Educational Focus

Child Trust Funds vs JISAs

In one of our recent newsletters, we touched upon JISAs, but did you know the precursor to Junior ISAs (JISAs) were Child Trust Funds (CTFs)

Children born between 2002-2011 are likely to have had a CTF opened by a parent. Probably more likely than those opening a JISA nowadays because

a) It was common to get information in the ‘maternity pack’ when mothers and babies left the maternity ward

b) The Gov contributed towards it at the point of opening (yeh, early Millennials also got free dough!)

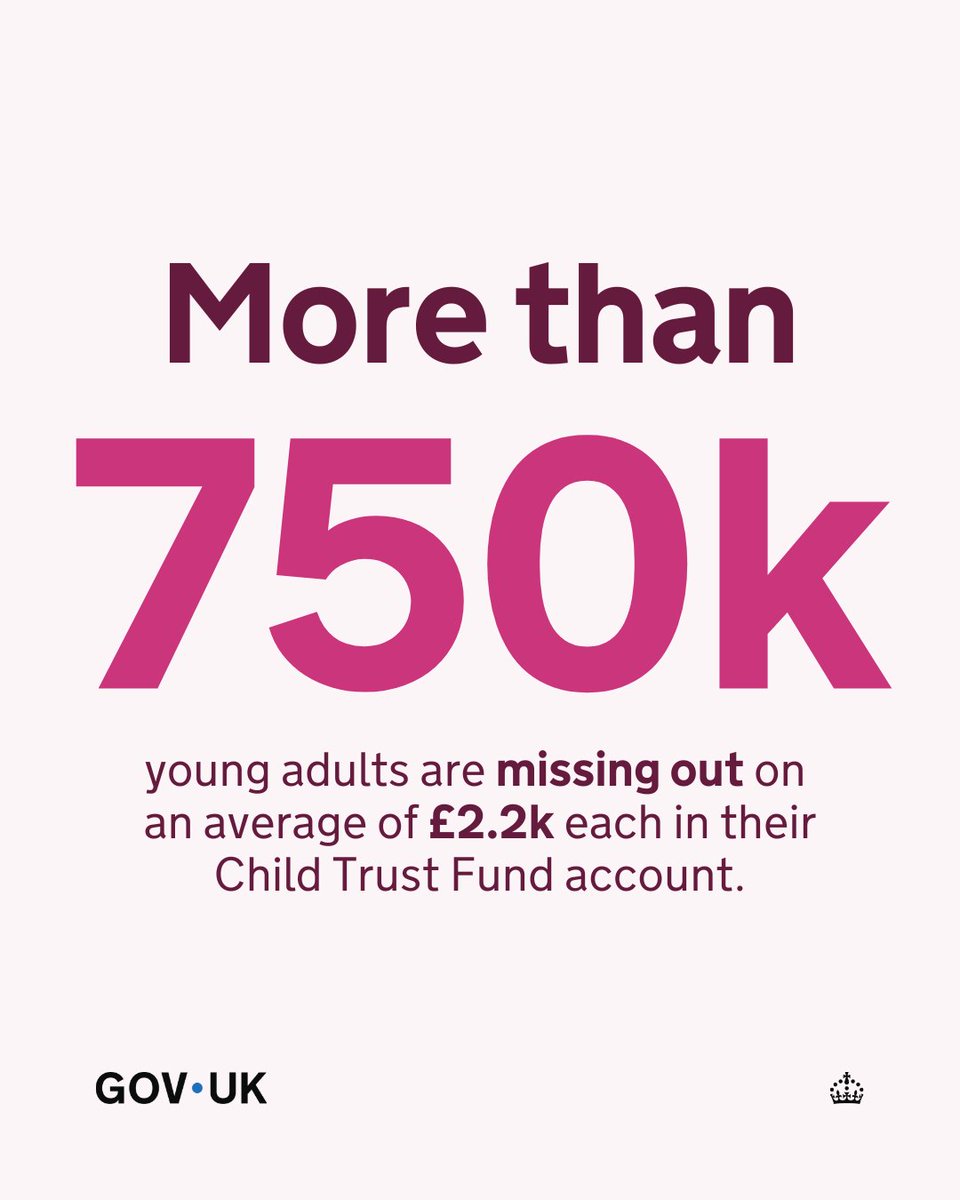

So what’s the news? As of April 2026, HMRC says there’s over 750k of these CTFs that remain unclaimed. That’s a likely scenario as it’s possible that parents opened the account to get the Gov top-up voucher - which also went into the CTF account - but then probably stopped contributing at some early point and genuinely forgot about it.

Apparently the average pot value is about £2,200.. Noice!

Well, if you happen to be one of them, this might be a letter from HMRC you’re happy to get. HMRC will be writing out to 21 year olds that have an unclaimed CTF.You can also check yourself if you have a CTF by using the Gov’s tool here

When CTFs came to an end, they were replaced by JISAs. Many parents may have chosen to convert their child’s CTF to a JISA, in which case you might not find the CTF using that tool.

Hey, maybe one day you can tell your current/future grandkids there was once a thing called a LISA… yeh that’s about to go through some major changes too, so stay subscribed to the newsletter to get the news when it drops.

The Cheapest Halal Pension in the UK

Two people. Same £400 a month for 35 years. Same Shariah compliant global equity fund. One ends up with £700,000, the other with £900,000.

The only difference is fees. And most UK Muslims have no idea what they're actually paying.

In our latest article, we break down the two fees you need to understand, compare what Wahed, PensionBee, Nest, AJ Bell, Trading 212, Aviva and the major workplace providers actually charge, and explain the hidden withholding tax drag almost nobody talks about, plus the one fund structured to eliminate it.

If you've never checked your pension fees, this is your sign. Thirty minutes today could be worth six figures by retirement.

https://www.nisba.co.uk/blog/cheapest-halal-pension

Halal or Haram? Why Caterpillar Got Both Answers

We checked Caterpillar on two of the most popular Shariah screening apps this week. Same screening criteria. One said halal. The other said haram.

So we went digging.

It turns out Caterpillar's financing arm earns around 6.2% of group revenue from interest, just above the 5% AAOIFI threshold. Most screening apps missed it, because automated screeners pull from financial APIs and broad industry codes rather than reading the annual report line by line.

And that's before you get to the ethics question. In August 2025, Norway's $2 trillion sovereign wealth fund divested its $2.1 billion stake in Caterpillar over the use of its bulldozers in Gaza and the West Bank.

Screening apps are a useful starting point, but they're a ratio test, not a conscience. This article unpacks what they actually check, what they miss, and why it matters.

Final reflection

I've been thinking more than usual lately. I left my job to pursue something in Islamic finance, and from where I'm sat there are really only three ways this ends. Nisba grows into a serious force in financial services, we help move Islamic finance forward, and I look back on the decision as one of the best I ever made. Or we just about survive, ticking along indefinitely. Or we crash and burn as an unsustainable business. Most days I think about all three.

The more people we educate, the more convinced I am that what we offer is genuinely valuable. But there's a problem. In a tightly regulated industry, where we play by the rules, we lose attention to people throwing out stock tips. We lose it to scammers shouting about overnight returns. We lose it to FX traders promising the world.

We don't promise you'll make money, because investing comes with risk. We teach you to invest through funds, and people assume they already know how to buy a fund, so what's the point? We focus on the understanding that lets you take informed action for the rest of your life, but people want the answer right now.

Our biggest challenge isn't the teaching. It's showing people why what we teach, and how we teach it, is worth their time when louder voices are offering shortcuts that don't exist. Let's see if we manage it.

Responses