The Cheapest Halal Pension in the UK: Shariah Compliant Pension Fees Compared

May 13, 2026

Imagine two people saving for retirement. Both contribute £400 a month for 35 years. Both are invested in a very similar Shariah compliant global equity fund. One ends up with around £700,000. The other ends up with £900,000.

The difference? Fees. (run the numbers yourself using the Nisba calculator)

Pension fees are the quietest, most expensive mistake most UK Muslims are making with their retirement savings. The good news: fixing it often takes about half an hour and usually costs nothing. This article breaks down what you're actually paying, who the cheapest halal pension providers in the UK are, and one hidden fee that almost nobody talks about.

Why halal pension fees matter so much

A 0.1% difference in fees doesn't sound like much. But over 35 years of compounding it can add £20,000 to your final pot. A full 1% gap? That's £200,000 or more on the same monthly contribution.

Your pension could one day be worth more than your house. A fee difference you wouldn't blink at on a £30 phone bill becomes life-changing when it runs every year on a six-figure pot. That's why this is worth thirty minutes of your time today.

The two fees you need to understand

When it comes to halal pensions, there are two main charges:

Platform fee. This is what the pension provider charges you for using their platform.

Fund fee. This is what the underlying Shariah compliant fund charges. For Islamic funds in the UK, these range from around 0.3% to just under 1%.

Add them together and you get your total fee. Sounds simple, except it rarely is. Some providers bundle the two together. Some hide one of them. Some only show you the breakdown once you're already a member of the scheme.

There can also be an annual management charge (a fixed pound amount that hits small pots disproportionately) and tiny transaction costs (typically around 0.02% per year, which you can safely ignore).

Your first step before doing anything else: log into your existing pension and find out what you're actually paying. You can't compare what you don't measure.

Workplace pension vs Halal SIPP

There are two main types of pension to know about:

Workplace pension. You're auto-enrolled, you contribute, you get tax relief, and crucially your employer also contributes. Never close this down if your employer is still paying in.

Self-Invested Personal Pension (SIPP). You open it yourself. You still get tax relief, but typically no employer contribution. SIPPs are generally cheaper than workplace pensions and give you more control over which Shariah compliant fund you invest in.

Most people can't simply swap their workplace pension for a SIPP because the employer contribution is tied to the workplace scheme. But you can often transfer out a large chunk of your workplace pension into a cheaper SIPP every year or two, while leaving the scheme open so contributions keep flowing. Old pensions from previous jobs are usually ideal transfer candidates.

A word of caution: some older pensions come with valuable guarantees or benefits. Always call your provider before transferring, or speak to a financial adviser.

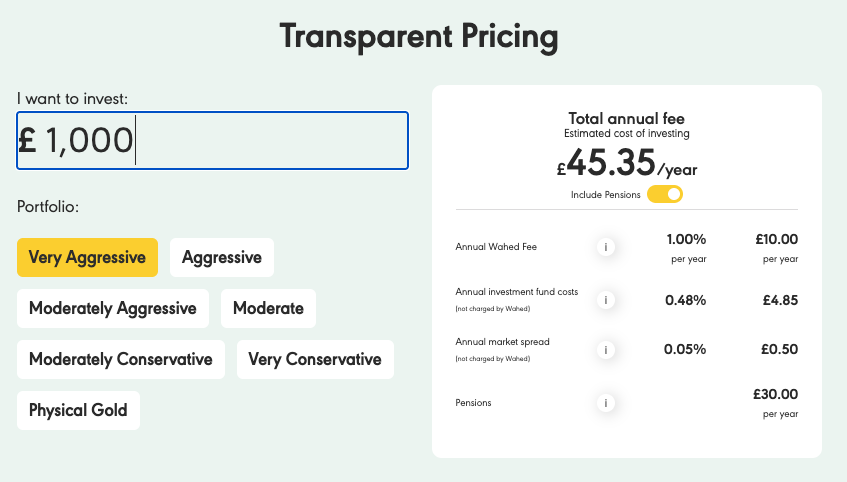

The most expensive halal pension: Wahed SIPP

Wahed is unique in being entirely Shariah compliant focused. You can't pick the wrong fund because they only offer halal options, which is genuinely valuable. But you pay for it. Their platform fee is around 1%, fund fees are slightly above market, and there's a £30 annual charge on top. All in, you're looking at around 1.5%, with the fixed £30 hitting small pots especially hard.

The mid-range: Aviva, Aegon, L&G, Standard Life, Scottish Widows

This is where most UK Muslims sit, often without realising it. These large providers typically charge 0.3% to 0.5% in platform fees, then layer on a fund fee that can range from 0.3% to 0.6% for what is essentially the same HSBC Global Islamic Equity Index Fund. All in, expect to pay 0.6% to just over 1%.

The frustrating part: fees vary by employer scheme, so two people with the same provider can pay completely different amounts. You have to check yours specifically.

Bundled-fee providers: PensionBee and Nest

PensionBee bundles their Shariah compliant fund at 0.95% all-in. Simple, but not cheap.

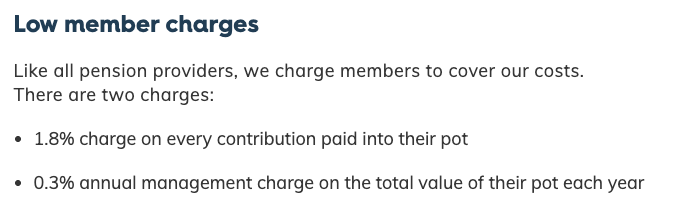

Nest is more interesting. Their all-in fee is just 0.3%, which is very competitive. But they charge a 1.8% contribution fee on every payment in. If you're actively contributing, that drag adds up. If you're doing a one-off transfer and no further contributions, Nest could be one of the cheapest options available.

The cheapest halal pensions: free SIPP platforms

This is where the savings live. Platforms like InvestEngine, Trading 212, and Freetrade offer SIPPs with no platform charges at all. Combine that with a low-cost fund like the HSBC World Islamic ETF at 0.3% and your total pension fee can be just 0.3%.

For context: that's a third of what most workplace pensions charge for essentially the same investment. AJ Bell and Hargreaves Lansdown also offer SIPPs with Shariah compliant options at around 0.25% to 0.35% platform fees, bringing you in just under 0.6% all-in.

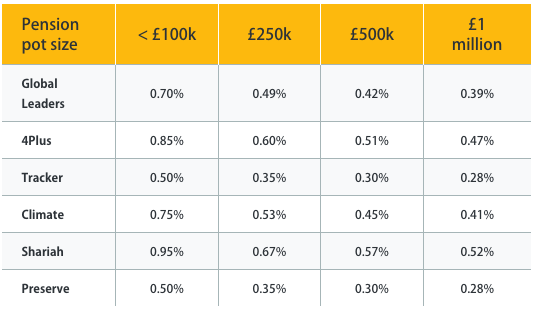

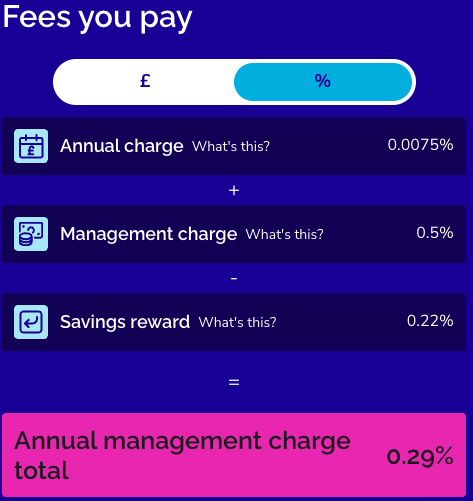

A special mention goes to The People's Pension, which offers fee rebates as your pot grows. At £50,000 invested the fee drops to 0.29%, and at higher balances it can go close to 0.2%, potentially making it the cheapest option for larger pots.

The hidden fee nobody talks about

Here's the one almost no one mentions. When a fund holds US stocks, it pays withholding tax on US dividends. You don't see this charge anywhere on your statement, but it quietly drags down returns.

The good news: pensions are exempt from this tax. The bad news: most Shariah compliant funds aren't structured to claim that exemption, so the fund pays it anyway on your behalf.

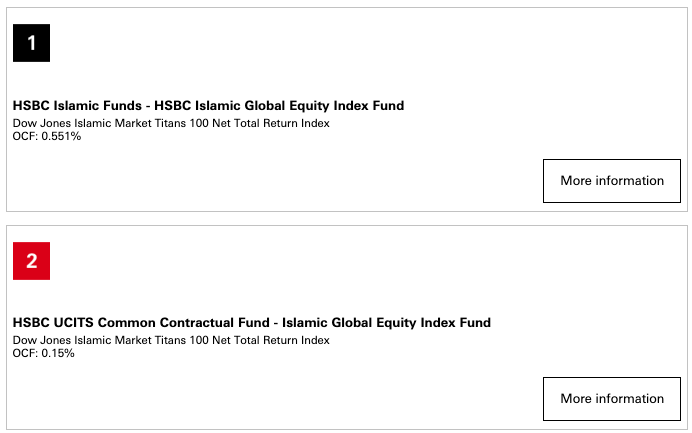

There is now a Shariah compliant fund structured specifically to eliminate this drag for pension investors: the HSBC Global Islamic Equity Index Fund in its Common Contractual Fund (CCF) version. It's not available in SIPPs but is offered by a small number of pension providers. Over decades, this saving can compound into a meaningful additional boost.

Your action plan

- Log into your current pension and find out the exact platform fee and fund fee you're paying.

- If your employer contributes, never close that pension. Keep it open and contributing.

- If you have old pensions from previous jobs, or are willing to do partial transfers, compare them against a SIPP with a 0.3% Shariah compliant ETF.

- Call your existing provider before transferring to check for any special benefits you'd lose.

- If you're unsure, speak to a qualified financial adviser.

See the video

Want help getting this right?

Halal pensions are one piece of a wider halal investing strategy. To see how it all fits together, grab the second edition of our free guide "6 Steps to Halal Investing" at nisba.co.uk/playbook. It walks you through goals, investments, asset allocation, account types, implementation, and ongoing refinement, all in plain English.

For a deeper, structured journey from beginner to confident halal investor, the Nisba Academy takes you through the full framework with worked examples and templates.

This article is for educational purposes only and is not financial advice. Pension fees and providers change over time, so always verify current charges with your provider before making decisions.

Learn more about Halal Investing

Stay up to date with halal investing

Join our mailing list for the latest insights, updates, and opportunities from Nisba.

We respect your privacy, no spam, ever.