A few weeks ago, the Fear & Greed Index was sitting in extreme fear. Markets were red, headlines were far from positive, and a fair few people I spoke to were quietly wondering whether to pull back, sit on the sidelines, or just stop checking their portfolios altogether.

Today, the same index is reading 67. Greed.

Nothing fundamental has changed in the world in those few weeks. The same wars are still being fought. The same uncertainty still hangs over interest rates, trade, and politics. What's changed is the mood. And the mood, as it turns out, is a much faster mover than the fundamentals ever are.

If you bought during the dip, well done. Genuinely. But I'd gently push back on the idea that you've cracked the code. Catching one dip well is not the same as having a strategy. The investors who do well over decades aren't the ones who time the bottom of every wobble. They're the ones who keep showing up regardless of where the index is sitting that week.

The harder skill, and the one almost no one talks about, is staying boring when everyone else is either panicking or celebrating. Most of investing is just refusing to be moved by either.

Contents

-

Nisba Updates

-

Halal Fund Performance

-

Top Halal Savings Rates

-

Fear & Greed Index

-

Platform Updates

-

Islamic Reflection

-

Competitions

-

Educational Focus

-

Article 1: The shining star of German fintech

-

Article 2: The youngest ISA millionaire

-

Final Reflection

Nisba Updates

The next cohort of the Nisba Academy begins tomorrow. In a few weeks inshAllah this group of people will have an automated portfolio working for them and the knowledge to back it up as they build it themselves. If you've been thinking about joining, secure your spot here.

Before that, we're running an intro webinar tonight for £3. It's a great way to get a feel for what we do and decide if the Academy is right for you. Worst case, you'll walk away with some useful insights for £3.

The first batch of the Nisba Playbook has officially sold out. A huge thank you to everyone who picked up a copy. The new edition has been sent to the print house and will be with us in a few weeks inshAllah. It has a new worked example, bonus chapters including crypto and a completely fresh look. We are so happy with how it’s turned out alhamdulilah - www.nisba.co.uk/playbook to preorder your copy

We'll be at the Modest Fashion Event in London on Friday 9th May. If you're around, come say hello, we'd love to meet you in person.

Some lovely news on our end, we've been nominated for Islam Channel's Community Business of the Year. Genuinely humbled to even be on the list. If you've supported us along the way, this one's partly yours too.

And finally, we have a TV show in the pipeline. We can't say too much yet, but it's something we've been quietly working on for a while. More on this when we're allowed to spill the beans, inshaAllah.

Halal Fund Performance

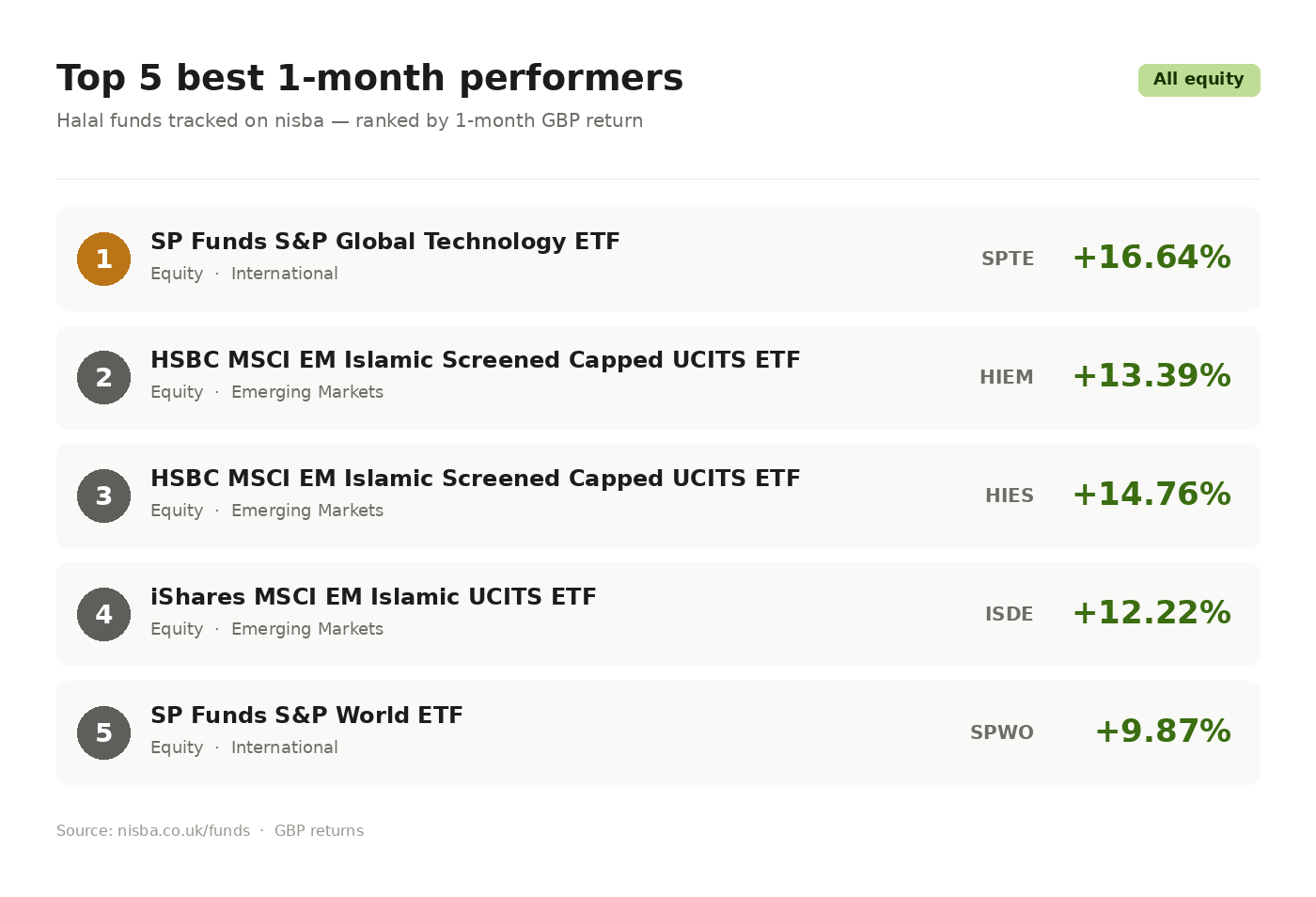

Top 5 Best 1-Month Performers

A strong month across halal funds, with only a handful posting negative returns. Emerging markets and global tech led the upside, though the top performer (SPTE) is only available to US investors, making HIEM the best accessible pick for UK investors. The downside was concentrated in sukuk, reflecting fixed income lagging the broader equity rally.

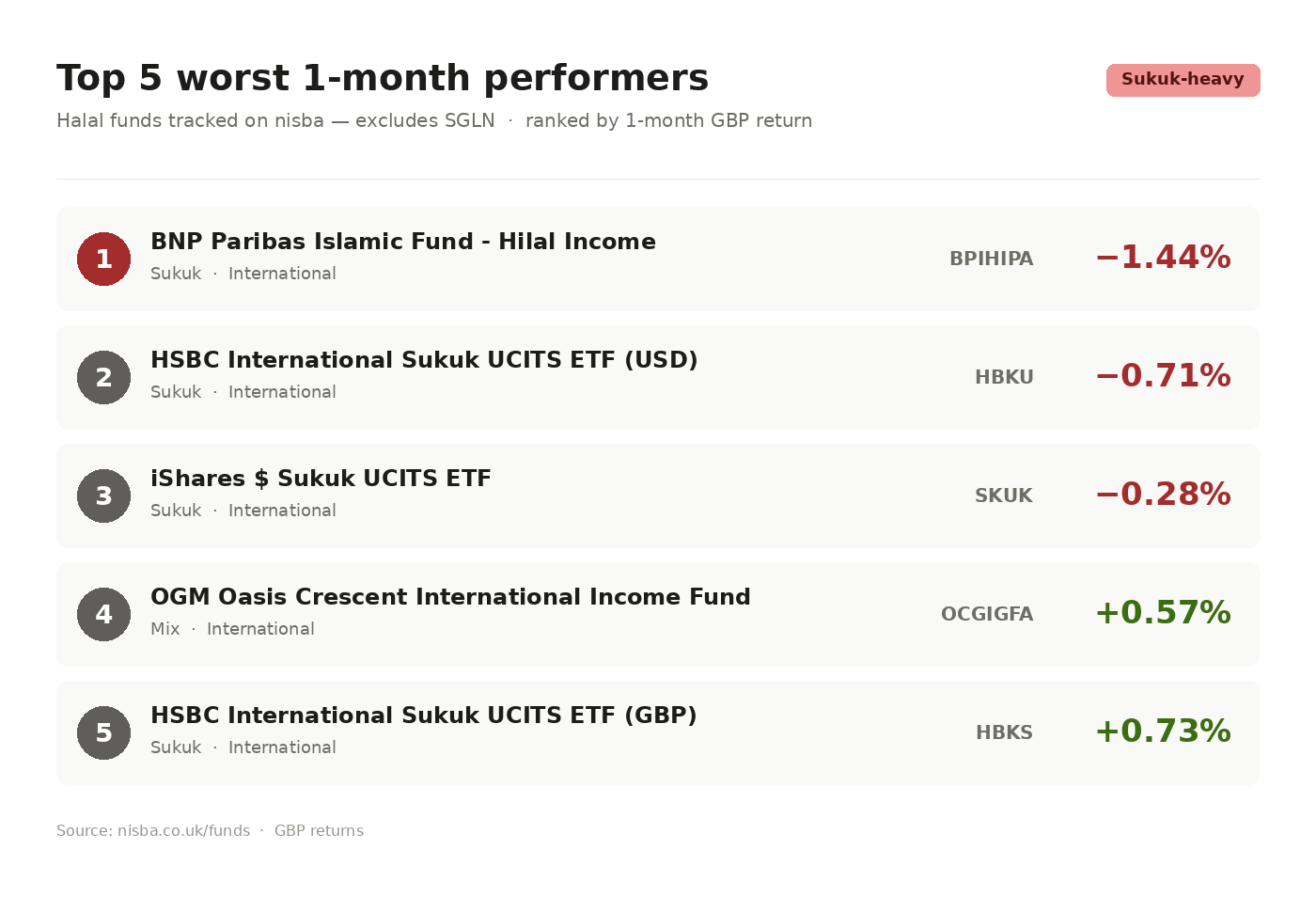

Bottom 5 Worst 1-Month Performers

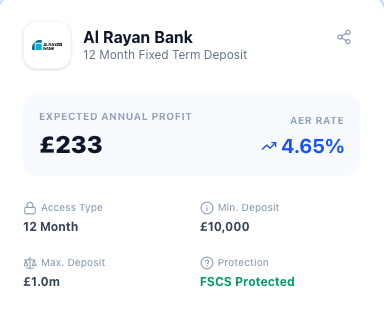

Top Savings Rate

Surprisingly enough, savings rates seem to have gone up again in recent weeks. The big caveat is that AlRayan who have boosted their rates, have also increased their minimum investment to £10,000.

So worth double checking the account before getting too excited and trying to open one up. Remember to check out all the savings accounts on the nisba website. However, you can access AlRayan via some aggregators so there could be a loophole there to minimum deposit amount.

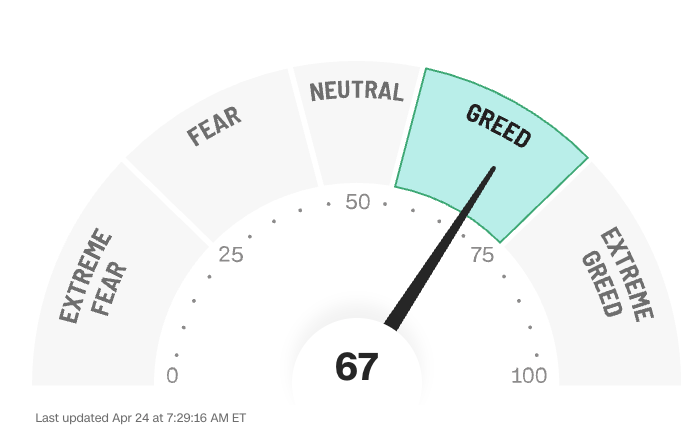

Fear and Greed Index

What is it? The Fear & Greed Index is like a mood tracker for the stock market. It looks at 7 different signals to give the market a score from 0 to 100, where 0 means investors are really scared, and 100 means everyone is feeling super confident and buying everything in sight.

Commentary: Currently the index is sitting at 67 - Greed. It’s funny how quickly things can change from almost extreme fear a few weeks ago to everyone happy and putting their money into investments like it can only go up.

It’s a reminder for long term investors, sometimes staying too close to the news can cause more harm than good.

PLATFORM UPDATES

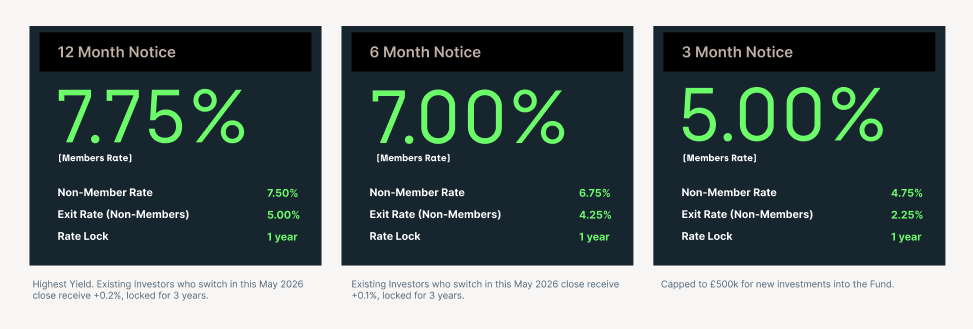

Cur8 Capital

The flagship GBP Income fund from the Cur8 (IFG) team is finally live, and it's a mixed picture. Returns have been steady and the fund has grown nicely, both genuine wins.

The shift worth flagging is on rates. The fund used to sit at 3 months notice as standard, and that's now the lowest tier at 5%. To get back to the kind of yield people were used to, you're looking at 7% on 6 months notice or 7.75% on 12 months. The good rates are still there, you're just giving up liquidity to access them.

Worth a think before adding fresh money in.

HSBC

We mentioned last time that HSBC has a new halal infrastructure fund coming. We've been invited to the internal launch next week and will report back properly next issue.

It's a nice change too, halal funds have always been split by geography, so having one focused on a single industry is a fresh take.

Pfida

Great news from Pfida, they've moved within the FCA regulatory framework. In the words of their founder Raza, "this means our products and communications now operate under enhanced regulatory oversight, whilst staying true to the ethical values we've upheld since day one."

To be clear, this doesn't mean investments or savings are FSCS protected. But it does add another layer of confidence in their model and the safeguards around it. We are planning an event soon so keep an eye out.

Halal Screener

The S&P 500 is up 8% over the last month. If you tracked the shariah compliant and boycott friendly version through the Halal Screener, your returns should be sitting in a similar range. There's a new fund available now too, with another one launching very soon.

Wahed

Wahed have updated their terms to make it clear they'll be using their own funds within their portfolios. Not really new news, more of a formal confirmation of what's already been happening.

Kestrl

We'll be hosting the Kestrl team in the coming weeks to get under the bonnet of their accounts and see whether this really can be the new Islamic current account people have been waiting for. Word is there's also an easy access Cash ISA with FSCS protection on the horizon, which would be a big deal if it lands.

Trading 212

The MWIM fund is now available in GBP on Trading 212. Worth noting because it covers both developed and emerging markets in one, and having it in GBP removes the currency friction for UK investors.

Lightyear

Lightyear have added 110 new ETFs to the platform, all with no order fees and priced in GBP, so no FX costs either. Two of them are shariah compliant, which on its own isn't huge, but it's another small step in the right direction for the platform. That makes 4 in total now.

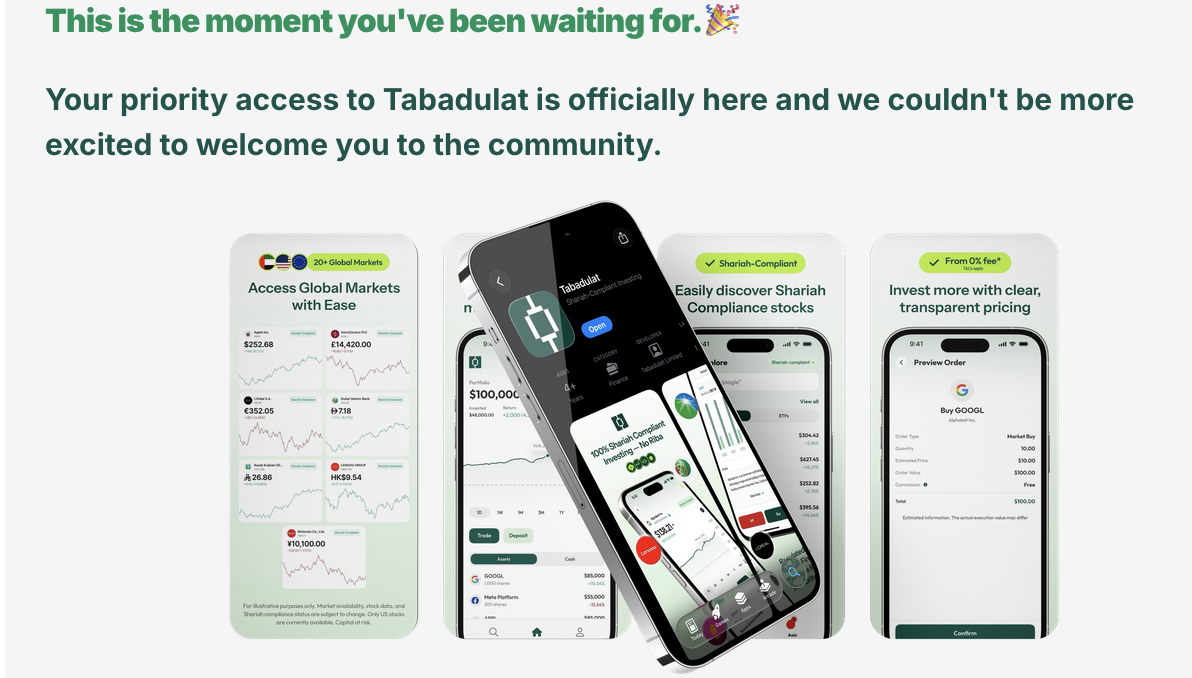

Tabadalat

The newest platform on the scene. Tabadalat have been building quietly for a while and have essentially created a shariah compliant version of Trading 212. You get free shariah ratings on individual stocks, and the platform won't let you buy anything that isn't compliant in the first place, which is a nice guardrail.

One thing to flag, they're based in the UAE, so we'll need to see how FX plays out and what the actual range of stocks and funds looks like. We'll have a proper play with it over the next few weeks and report back inshAllah.

Islamic Reflection

I've been thinking a lot recently about how quickly time moves, and how rarely we stop to notice it. One day rolls into the next, weeks become months, and somewhere in the middle of it all, we forget that this life is finite.

In Islam, time is one of the few things Allah swears by in the Quran. By the passage of time, surely mankind is in loss. It's a short ayah but it lingers if you let it. The fact that it opens with time is not random. Time is the one resource we all share, the one we cannot earn more of, and the one most of us treat as if it's unlimited.

What struck me this week is that we tend to measure our lives in achievements. Did I hit the goal, did I close the deal, did I tick the box. But the Quran flips it. The measure isn't what you produced, it's what you did with the time you were given. Belief, good deeds, truth, patience. That's the checklist.

I think we sometimes assume that being busy means being productive, and being productive means being successful. But you can be all three and still be drifting if the direction isn't right. A boat moving fast in the wrong direction is still going the wrong way.

Maybe the real question isn't how much we got done this week, but whether any of it actually mattered in the way that lasts.

Competitions

We've had a few competitions running recently. Two lucky winners bagged a hoodie each from our feedback survey, but they still haven't claimed their prize, so check your junk mail just in case it's you.

Congratulations to Moatasem, our winner of the Time Hoppers challenge.

Educational Focus

Pension News

We all know the minimum age you can access your private pension (such as a SIPP) is rising from 55 to 57 from 6th April 2028, right? Well you should do!

But what about those folks that will be 55 or 56 on 5th April 2028?

Well, HMRC has just confirmed for those born between April 6, 1971 and April 5, 1973 they will not be able to:

• Move additional funds into drawdown after April 2028

• Take further tax-free lump sums

• Start a new annuity or defined benefit pension

Instead, they will be forced to pause any phased retirement strategy until they turn 57.

That doesn't mean you can't take your pension benefits at 55 or 56 before that date. But after 6th April 2028, you'll have to wait until age 57 before you can take additional/new benefits . Ba Humbug!

Article 1: The shining star of German fintech

When you hear of a German product, maybe you're like me and you think efficient, trustworthy, reliable. That's the brand Germany has built over decades. The home of Volkswagen, Adidas, Aldi, BMW. Names that carry the weight of "they know what they're doing."

Wirecard fit that mould perfectly. A Munich based payments company that became the shining star of European fintech. By 2018 it was worth more than Deutsche Bank. It was promoted into the DAX 30, replacing Commerzbank, an institution that had been around since 1870. The old guard out, the future in.

Then in June 2020, Wirecard admitted that 1.9 billion euros sitting in its accounts probably did not exist. The share price fell by 98 percent in a matter of days. The CEO was arrested. The COO disappeared and is still on Europol's most wanted list. Within weeks, it became the first DAX company in history to file for insolvency.

Investors who held Wirecard directly lost almost everything. But many people who never picked Wirecard also took a hit, simply because they held broad European index funds that owned it. When a company is in the index, you own it by default.

This isn't a one off. Every generation has its version. Kodak invented the digital camera and then collapsed under the weight of the very technology it created. Nokia owned the mobile phone market, until it didn't. Blockbuster could have bought Netflix for fifty million dollars and instead became a punchline. Each was, at its peak, considered untouchable.

The lesson is not to avoid investing in great companies. It's to be honest about what you actually know. No business is too big, too iconic, or too modern to fail. Concentration in a single name, no matter how shiny, is a bet on a future none of us can see clearly.

From an Islamic perspective, this sits well with how we're encouraged to approach wealth. Avoid excessive risk and be clear about what you own. Shariah screening would have flagged Wirecard's financial ratios long before the fraud surfaced, not because the screens predict scandals, but because the discipline of looking under the bonnet tends to keep you out of places you shouldn't be.

Article 2: The other side of the same coin

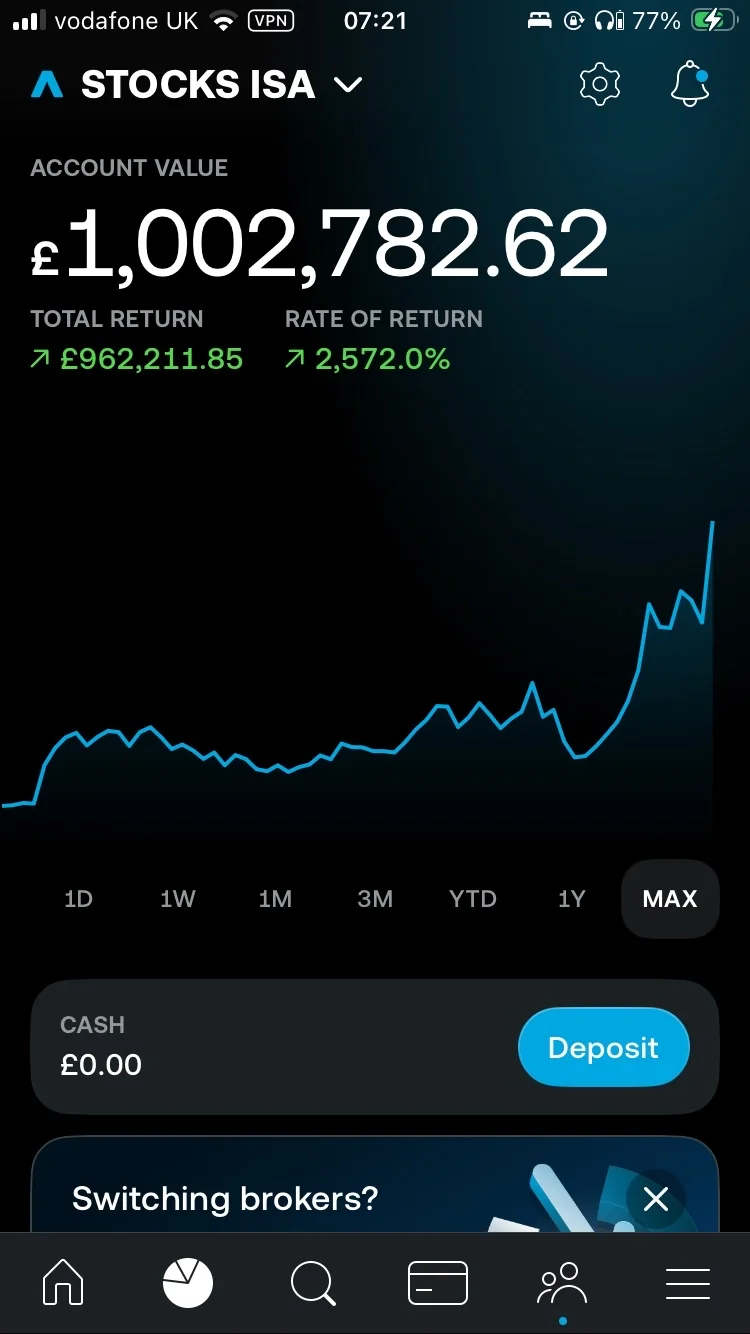

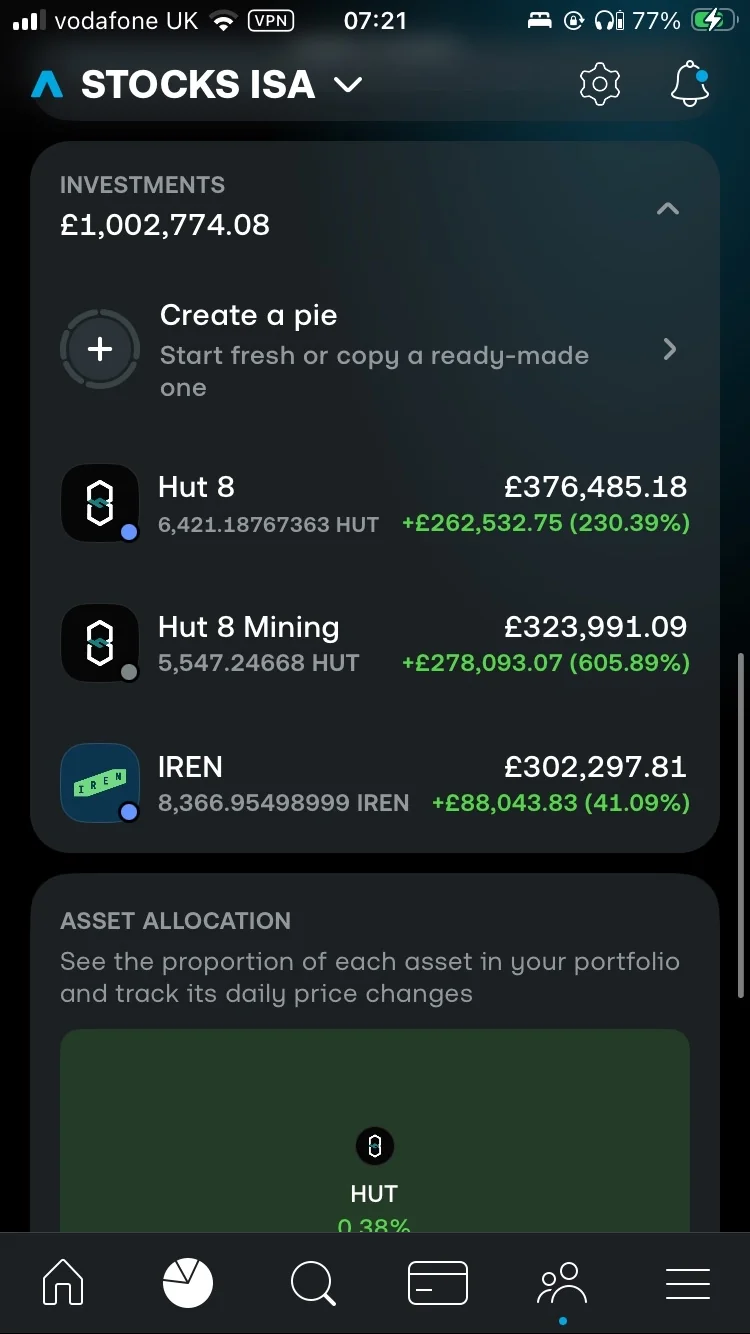

A post went viral on Reddit this week. A young investor sharing a screenshot of his Trading 212 ISA, just over one million pounds, claiming to be the youngest ISA millionaire in the UK. The numbers are eye watering. Hut 8 up 230%. Hut 8 Mining up 605%. IREN up 41%. Three positions, all in the same corner of the market.

Fair play to him. He took a view, held his nerve, and it paid off in a way most of us never will.

But it's worth pausing on what we're actually looking at. Three stocks, two of them essentially the same company, all riding one narrow theme that's been on a historic run. This isn't a case study in disciplined investing. It's a bet that happened to come good.

This is the part survivorship bias hides from us. For every screenshot of a million pound ISA built on three names, there are thousands of portfolios built the same way that are now down 60, 70, 90%. We don't see them. They don't post. They quietly close the app and move on.

And there's a harder question lurking underneath. If you've turned a small sum into a million pounds through three concentrated positions, what do you do now? The same conviction that got you in is the same conviction that will tell you to hold. And the market has a way of humbling people who confuse a good outcome with a good decision.

For the rest of us watching, the takeaway shouldn't be "I need to find the next Hut 8." It should be a quiet reminder of how easily a single screenshot can warp our sense of what's normal, what's repeatable, and what's actually wise.

The path that builds lasting wealth tends to look much more boring. Diversified. Patient. Unremarkable on any given day. It doesn't make for a viral post. But it works for far more people, across far more futures.

Be inspired by the headline. Just don't mistake it for a strategy.

We actually invested into IREN as part of the nisba competition. It was a pretty wild ride, even with £500.

Final Reflection

One thing I've been sitting with this week is how easy it is to confuse motion with progress.

When you're running a business, or even just managing your own money, there's always something to do. Another email to send, another spreadsheet to update, another idea to chase. And it can genuinely feel productive. You end the day tired, which we often take as proof that the day was well spent.

But tired isn't the same as meaningful. You can spend a whole week running and end up exactly where you started, just more exhausted. I've caught myself doing this more than I'd like to admit.

What I'm slowly learning is that pausing isn't the opposite of progress. Sometimes it's the thing that makes progress possible. Stopping to ask whether what you're doing is actually moving you forward, or whether it's just keeping you busy enough to feel okay about not asking the bigger questions.

It's uncomfortable to sit still long enough to think honestly. But I think that discomfort is usually where the most useful answers live.

That's my reflection for this week. Again, more for me than anyone else.

Adel, Ahmad and the nisba team

Responses