Todays letter:

- Don't look down: a comment on rapid rises and fallers

- Another halal fund

- Sukuk vs bond performance - by Akbar Muminov

- New provider of Halal

'mortgages'HPP - War and asset prices

- Nisba news

- Outro

There are times in investing when things rise faster than you expected.

You might assume gold could rise 8–10% per year over the long run. Then suddenly you’re up 35% in one year… and another 40–50% the next. It feels incredible. Confidence rises. Risk feels distant.

But time has a funny way of making us forget that markets move in both directions.

A 10% fall from 100 takes you to 90.

A 10% fall from 1,000 takes you to 900.

The higher something climbs, the larger the drops feel. And when prices rise quickly, they tend to attract fast money, investors chasing the latest trend. That money moves in quickly, and often leaves even faster.

History shows that assets that have risen sharply in a short space of time are often the most vulnerable to sharp reversals. That doesn’t mean they will fall tomorrow. It simply means expectations need to be realistic.

And here’s the important perspective: if you’ve been investing for years, even after a sharp pullback, you are probably still well ahead. That is the power of time in the market. Compounding works quietly in the background through good years and difficult ones.

This rush of money into new 'trendy investments' has reared its head again as over the past few days I’ve been asked multiple times how to invest in oil.

Chasing whatever has just moved is rarely a strategy. It’s a reaction.

If you’re investing because something has just soared, be ready for the moment you have to look down. Markets that rise fast can fall faster.

Investing based on trends can be fun, but that’s not the Nisba way.

New Shariah-Compliant Fund: MWIM

Soon, us Muslims may be spoilt for choice. There’s a new halal fund on the block: Invesco MSCI ACWI Islamic M-Series UCITS ETF Acc (MWIM). Catchy name, I know.

This is the second Islamic fund from Invesco, the first being IGDA, their developed markets ETF, which has grown to around $1.2bn in size. It’s been a successful entry into the Islamic investing space for Invesco, so launching what looks like a “better” version makes sense.

When I say better, I’m not necessarily talking about performance.

I mean:

- Lower fees: 0.35% vs 0.40% for IGDA

- Dividend purification handled for you

- Transparency on purification, with proceeds going to UNICEF

It’s also more globally diversified. MWIM has around 62% in the US, compared to roughly 77% in IGDA, and includes exposure to markets like Taiwan, which IGDA doesn’t meaningfully cover.

The fund is already available on AJ Bell, and we expect it to appear on other platforms soon.

Sukuk vs bond return by Akbar Muminov

Sukuk is often described as the Islamic equivalent of a conventional bond - and for good reason.

It sits in the same part of a portfolio. It is issued by governments and large companies. It is designed to provide regular income and preserve capital. Structurally, however, it differs in one important respect: a conventional bond pays contractual interest, while sukuk is structured around ownership of assets or profit-generating activities, meaning returns are derived from profit rather than interest.

From a faith perspective, that distinction is fundamental. However, from the perspective of an investor looking for bond-like returns, the question is: how does sukuk’s performance actually stack up against conventional bonds?

What my research found is that recent data shows that the two move largely in tandem. Over the past year, global investment-grade sukuk delivered a return of 7.94%, compared to 8.56% for global investment-grade bonds. Over three years, though marginally sukuk outperformed, its performance was still broadly in vicinity of bonds’, 4.63% p.a. vs 3.19% p.a. respectively.

Performance during stress periods reinforces the comparison. In 2022, when global interest rates rose at the fastest pace in decades, global bonds fell -16.25%, while global sukuk declined -12.12%.

The similarity is not accidental. Both markets are predominantly investment-grade, meaning relatively low default risk. Both generate most of their return from predictable income payments rather than rapid capital growth. And because both promise a stream of future cash flows with repayment at maturity, their prices are sensitive to changes in market interest rates. When rates rise, the present value of those future payments falls - whether those payments are labelled “interest” or “profit.”

Where modest differences emerge is in market composition. The sukuk market is more concentrated in Gulf countries and Malaysia, with heavier exposure to sovereign and quasi-sovereign issuers. This regional tilt means performance can be influenced at the margin by oil prices and fiscal conditions. In recent years, that exposure has been supportive: sukuk’s stronger three-year outcome reflects the relative resilience of Gulf sovereign credit profiles, bolstered by elevated energy revenues during the rate shock period.

Looking ahead, correlation with conventional bonds is likely to remain high - and may even increase - as more countries issue sukuk and the range of structures expands. As the issuer base diversifies and integrates further into global capital markets, sukuk becomes increasingly influenced by the same macro drivers: interest rates, inflation expectations and credit spreads.

That said, regulatory developments are worth watching. Ongoing refinements to AAOIFI Shariah standards particularly around asset ownership, risk transfer and purchase undertakings - could materially affect how sukuk are structured. If tighter requirements reduce the use of mechanisms that replicate conventional bond economics, sukuk may carry greater asset-level risk and therefore return than bonds.

For now, however, the evidence is clear. Sukuk behaves economically like investment-grade fixed income. The structure is different. The performance is largely similar.

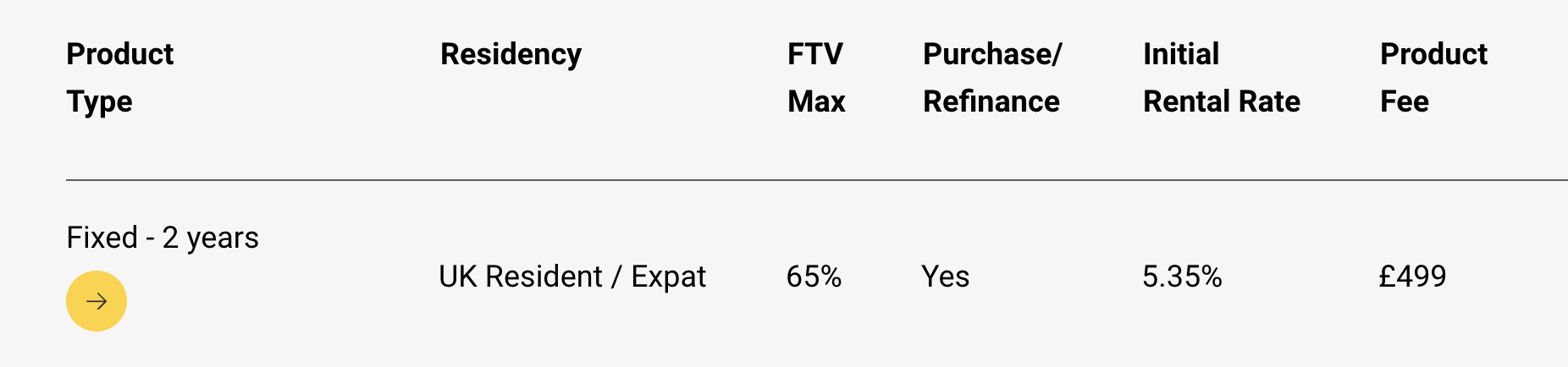

The latest provider in halal mortgages HPP

Have you heard of 'Offa' before? They've been doing Shariah-Compliant property financing for almost a couple of years, but it has been limited to buy-to-let and bridging loans. Now they've opened their doors to those who just want to buy a house to live in.

They claim on their site, you can buy a house with a 5% deposit, finance at 7x your earnings, and have it all being 100% sharaih compliant. Their rates at the moment go as low as 5.35% for a 2 year fixed with a £499 product fee.

Today we aren't getting into the argument of how halal are halal home purchase plans, but its nice to see the sector is growing and getting more competitive.

When wars happen prices go...

The Iran war has begun. It seems Trump is struggling to clearly explain why now was the moment to attack, but regardless of the reasoning, here we are, war it is.

Going Up.

The clearest impact so far has been on oil and gas prices. Iran is a key player in the global energy market, and conflict in the region disrupts both production and transportation. When energy supply feels uncertain, prices tend to rise. That’s exactly what we’re seeing.

Going Down.

The second obvious reaction is in equities. Markets have dipped and may continue to do so. When you buy a share, you are effectively buying a slice of a business. The value of that business depends on how much money it is expected to make in the future. That, in turn, depends on stable trade routes, predictable energy costs, consumer confidence, and political stability. When those variables suddenly become uncertain, the price investors are willing to pay falls.

Up and Down.

Volatility isn’t limited to stocks. The other day, Bitcoin jumped around 7% in under an hour, unusual at times like this. More recently, silver has swung sharply up and down within the same day. Gold has shown similar patterns.

Some view assets like gold, silver, and even Bitcoin as safe havens, “if the world goes mad, at least I have this.” But very few assets escape short-term volatility. In the long run, so-called safe havens may prove resilient. In the short run, they can still be pulled around by fear, speculation, and uncertainty.

How this unfolds will likely depend on how long the conflict lasts and how far its economic impact spreads.

Nisba news

Nisba on Linkedin

We now have a LinkedIn series which covers the different providers of halal investments. Previously, we have covered Nester and Bayuti. This week, we are covering the Wahed robo-advisory service. Check it out here: https://www.linkedin.com/company/nisbainvest/

If you have any companies you'd like us to cover, let us know.

Nisba Podcast

For and against investing for your kids’ ISA or JISA. Check out the first episode of our podcast on Spotify.

Check our the first episode of our podcast on Spotify.

Our video with NZF

This video doesn’t really have anything to do with how to calculate Zakat, but it covers interesting topics like: how much Zakat does NZF give out to people in the UK who are in need? Do we have an effective Zakat system? Should we give locally or internationally? Watch here.

A little questionnaire for those outside the UK

Are you investing in a halal way from somewhere other than the UK? We would love to know the details so we can update our fund list and provide better insights for our audience. If you can help us by answering a few questions, we would be most appreciative. Answer here: https://forms.gle/q1Q4gmJnJQugwbsy5

Nisba is raising money for orphans in Gaza. Calculate your Zakat and give!

Outro

From an investing perspective, this week may be a tough pill to swallow, with some significant market drops. But in the grand scheme of things, this wealth was never truly ours, it is simply entrusted to us for our short time in this dunya. Passing the test is not based on how much you accumulate.

Responses