I have seen some crazy times in markets. So many times people screaming that the market is overvalued, it's frothy, we are at a top. You know what, maybe this time they are right. Maybe they aren't though.

What I see today is a transformative technology rippling through the world. Perhaps this will be a golden era for investing, as companies become leaner, costs fall, and profitability improves. Productivity growth could explode in ways we haven't seen before.

Even if all of that is true, it doesn't necessarily mean markets go up from here. A few bad days can trigger selling. Selling can trigger panic. Panic can trigger a crash. And in hindsight, people will say it was obvious. Everything was overvalued. This was clearly bubble territory. Greed had reached fever pitch.

So let's say you've decided the market is too high. You have £10,000 in equities and you sell today.

Imagine you got it right. The market drops. Now comes the harder part, getting back in. When things are falling hard, fear keeps you on the sidelines. When markets start to recover, they can jump 4 or 5% in a single day, and you tell yourself you'll wait for the next dip. The dip doesn't come. Or it does, and you're still too nervous to move. Meanwhile you're refreshing your screen, watching every tick, second-guessing every day.

That is a lot of stress for something that may not even work.

If you have never tried timing the market, here's a thought. Wait for the next significant dip, whenever it comes, and try it. See how it feels in practice. Most people find it far harder than it looks from the outside.

If sleeping well is your priority, and you have a plan in place, the best thing to do during a downturn is close the app. You said when you started investing that you weren't going to touch this money for five years. So why does this month's valuation matter? Next month's? It doesn't. The plan hasn't changed. The timeline hasn't changed. The only thing that changed is the number on the screen, and that number will move again.

Contents

-

Nisba updates

-

Top halal fund performance

-

Top savings rate

-

Fear and greed index

-

Platform updates

-

Islamic reflection

-

Educational focus: Goodbye LISA / T212 SIPP / What happens when a stock turns non-compliant

-

Final reflection

Nisba Updates

-

The advisory service is now live alhamdulilah, under the brand Ansari Financial Planning, with Ahmad as the advisor. If you believe you could benefit from advice, minimum fees and capital requirements do apply, please confirm by replying to this email so we can share your details with Ansari and Ahmad will be in touch.

-

Also, we'll be at Muslim Tech Fest this weekend inshAllah at Booth 21 in the start-up section. Come say salaam.

-

And on Thursday we break down why your Trading 212 pie might be built all wrong

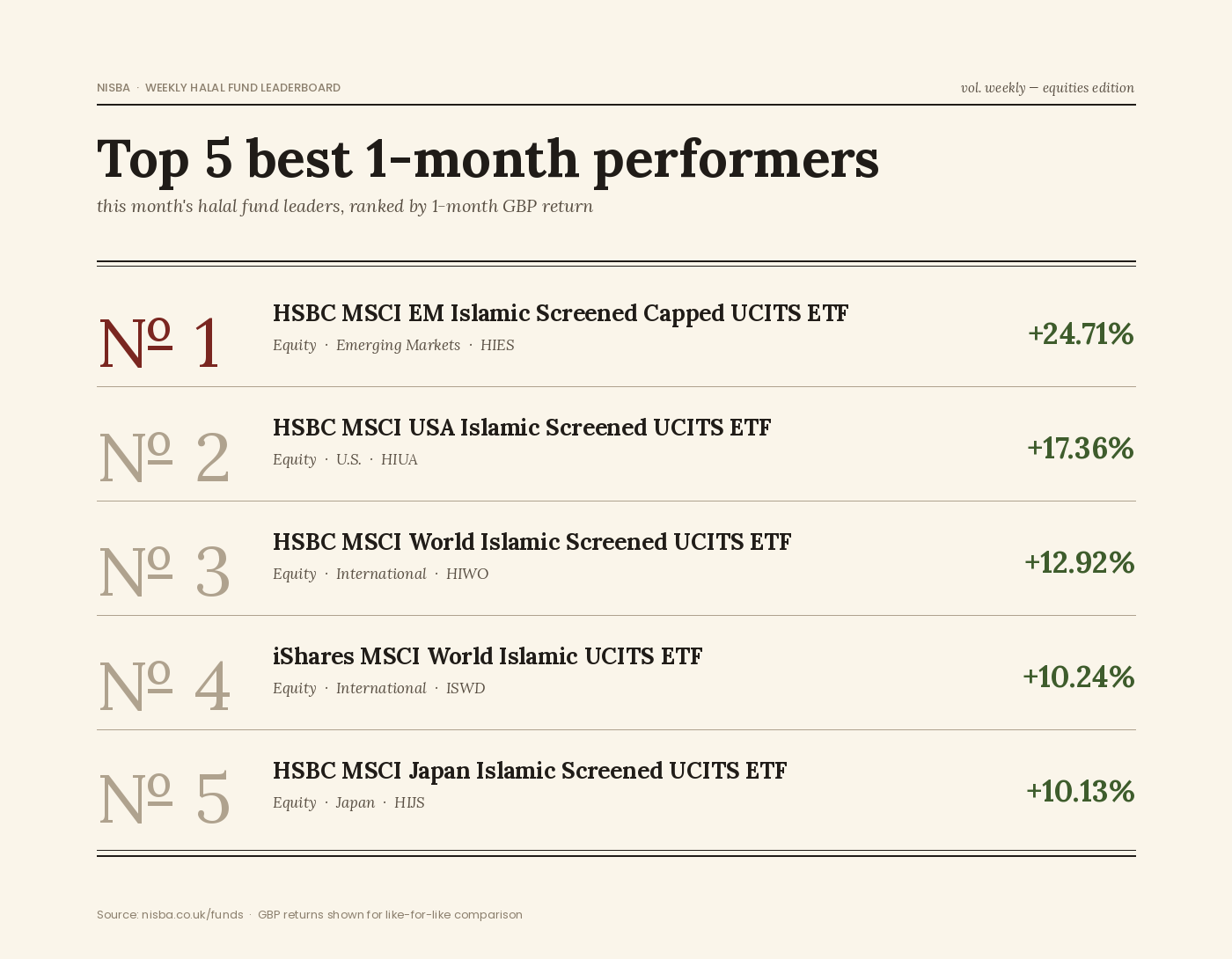

Top Halal fund performance (1 month)

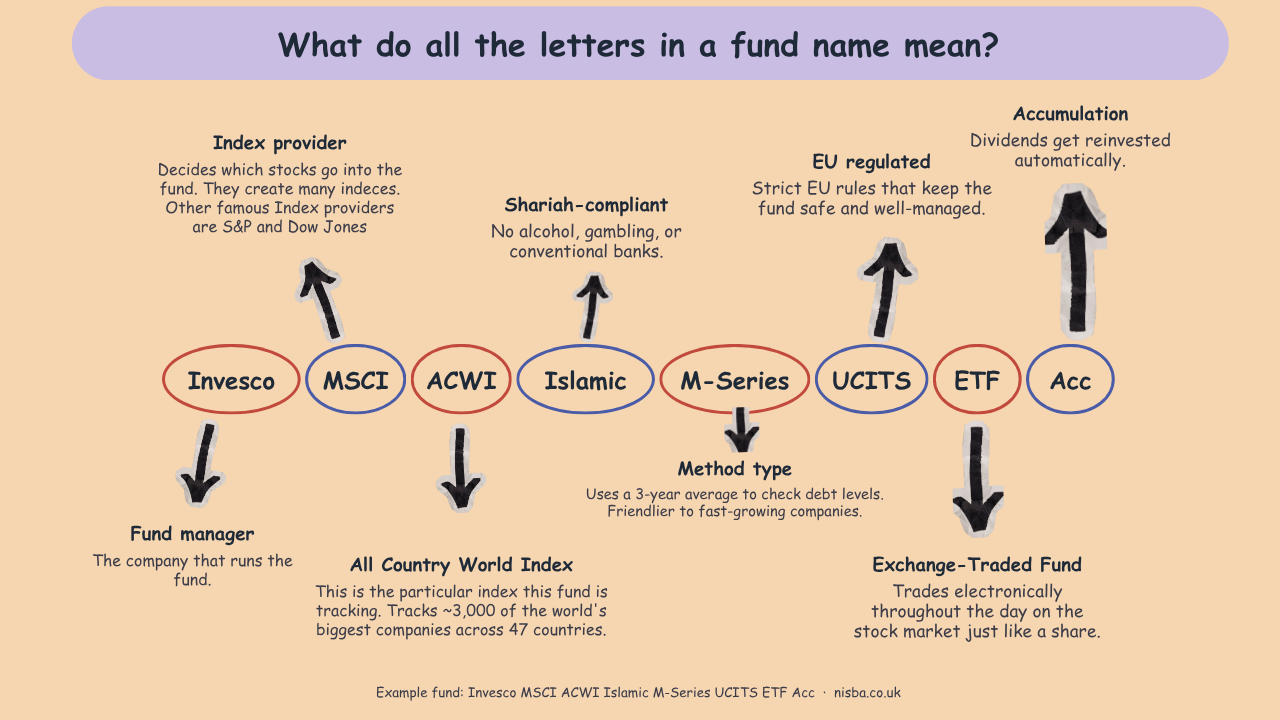

Before we show the top and bottom performers, I thought it might help to quickly dissect the different parts of a fund name so you can make sense of what you're seeing. Hope it helps

A clear divide this month: equities ran the table while crypto and metals took a beating. HSBC dominated the top with four of the five winners, led again by emerging markets and joined by the US, global and Japan. On the other side, Bitcoin took the biggest hit, with palladium, platinum and gold following it down.

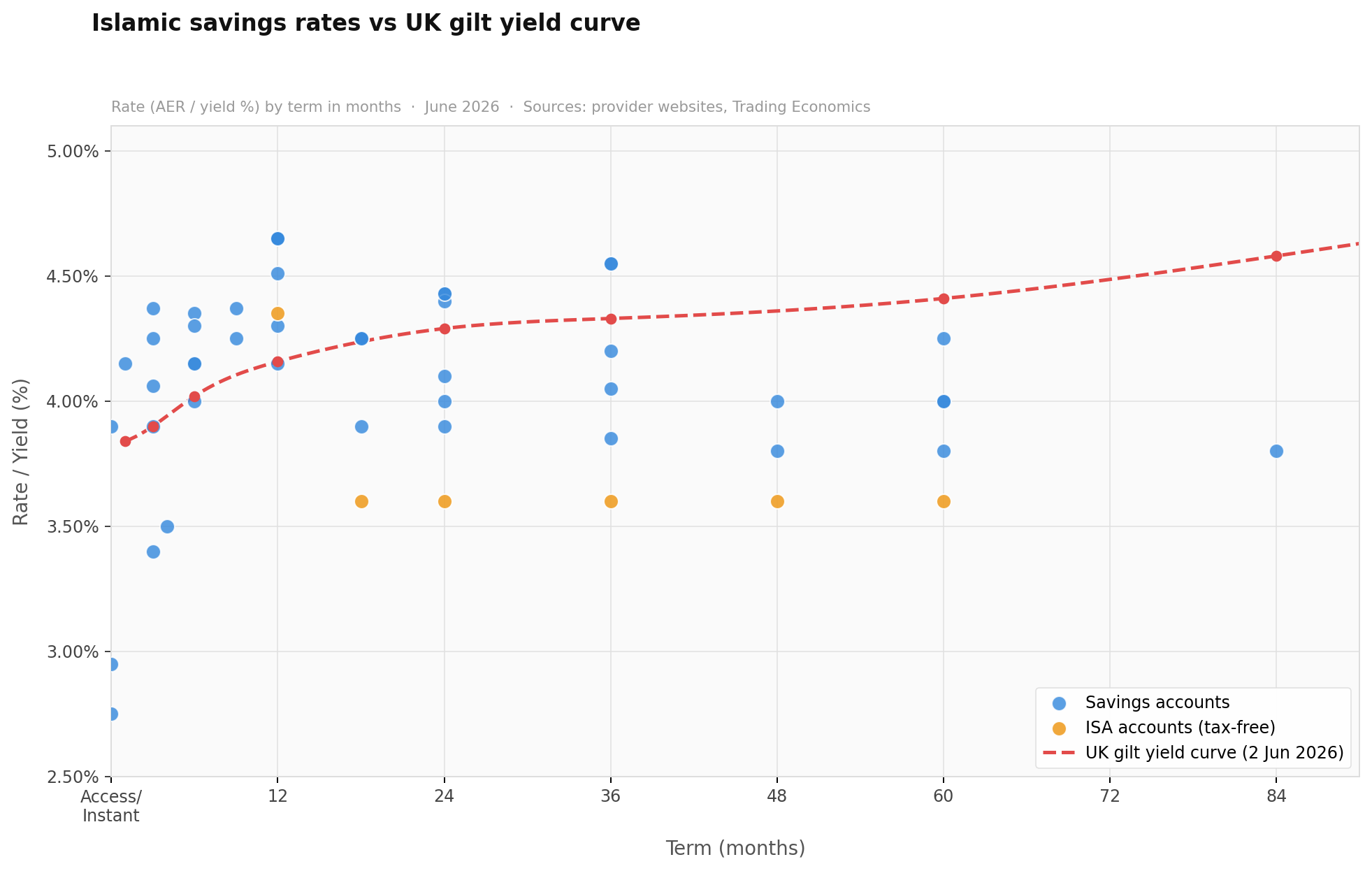

Top savings rate

- 1 year: BLME, QIB and Al Rayan all come in at 4.65%.

- 90-day notice: BLME at 4.37%.

- Easy access: 3.90%, QIB via Raisin.

Check our our recent article on Islamic savings accounts and their rates of return to learn more.

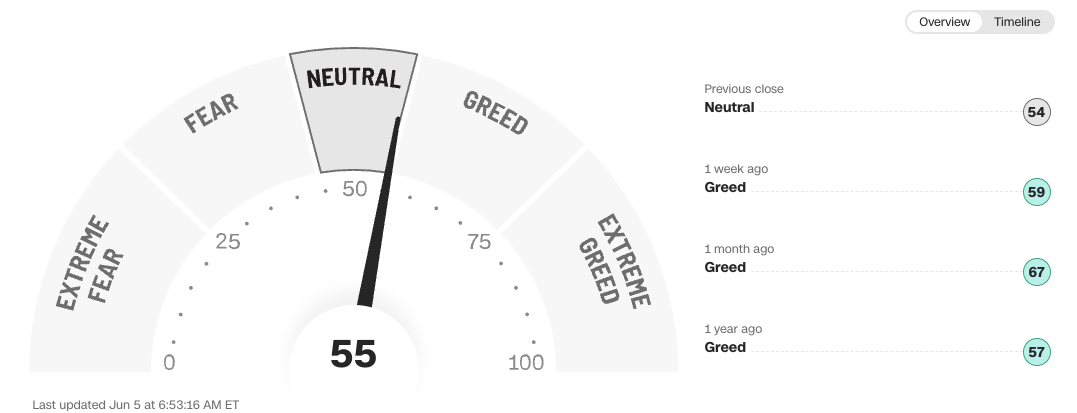

Fear and Greed Index

Sitting at 55, interstingly as this is lower than last week but there was another positive week of returns.

Platform updates

If you are an Islamic finance provider or aware of a relevant update, please let us know of anything exciting in the market.

-

HSBC Sukuk Fund has dropped its fees from 0.40% to 0.37%.

-

There is a new actively managed Islamic equity fund, this time from Baillie Gifford, which has been running behind closed doors for three years and is now available on some platforms, including Hargreaves Lansdown.

Islamic reflection

I've been reflecting recently on the fact that it's been almost three years since the genocide in Gaza began. And I feel ashamed to admit it, but I've become largely desensitised when videos come up on my feed. Sometimes I pause, sometimes I react but then I keep going. That sentence alone is hard to write, but I think it's important to say it honestly.

I think it comes down to the softness of the heart, or the slow loss of it. The Prophet ﷺ used to weep when reminded of the suffering of others, and here we are, watching it in real time, and somehow still managing to carry on with our day untouched. That's not something I want to make peace with.

So I'm trying to put some effort back into making better dua. Not the rushed kind we throw in at the end of salah, but the kind that actually comes from somewhere. I've started listening to a book called The Power of Dua, hoping it helps me reconnect with what I think I've slowly let slip. I'll keep you updated on how it goes.

Educational focus

Article 1: Goodbye LISA, hello First-Time-Buyer ISA

In our email last month we said we would keep you abreast of pending changes to the LISA. Here is what we are hearing so far, pending the necessary legislative changes:

-

It will be called a Help to Buy ISA.

-

It will strictly be for home purchases (though you probably guessed that from the name).

-

It cannot be used for retirement, that is what SIPPs are for.

-

It removes the age limit.

-

The withdrawal penalty has been removed.

-

You only receive the 25% bonus at the end, at the point of purchasing your first home. This means you miss out on the power of compounding that bonus each year, as you would under the LISA.

-

The target launch date is April 2028.

You cannot open a new LISA once the new product launches, but if you already have one open you can continue investing into it under the existing rules.

Opening a LISA with just £1 establishes your account, and HMRC has confirmed that the opening date is the date of first subscription. You can increase contributions later.

As a reminder, the problems the LISA was designed to address include the complexity of its rules: age limits, dual purpose (retirement or first-time buyer house purchase), withdrawal penalties, and house purchase price limits. There will of course be winners and losers from these changes.

Article 2: T212 SIPP, the good and the bad

Probably the most anticipated platform launch across the retail finance sector over the past six to eight months has been Trading 212's SIPP.

It had been in the works for some time, but this week we have been hearing that many more of our Nisba community have been able to get their hands on opening their SIPP.

As a reminder, a SIPP (Self-Invested Personal Pension) is a tax-efficient wrapper that allows you to plan and save for retirement. There are rules around how much you can contribute and when you can access the money, watch our video on SIPPs here.

The biggest benefits are the tax relief on contributions and the fact that a portion is tax-free when you come to access it.

SIPPs have been offered by several platforms for a number of years, but T212's entry has shaken up the market a little, as we have seen over recent months with providers like Hargreaves Lansdown and Wahed reducing their fees. We are all for healthy competition.

So what is good about the T212 SIPP? Similar to T212's other products, such as its Stocks and Shares ISA, there are no fees or commission for buying and selling shares, and they have retained the ability to create their own pies.

What to be aware of:

-

As with their other products, T212 offers ETFs but not index fund favourites such as the HSBC Global Islamic Equity Index Fund.

-

We found it was not straightforward to disable the earning of interest on uninvested cash held in the SIPP. This is an odd omission given the option exists in their other products, and it may be addressed in a future update.

-

The T212 SIPP can only be funded by personal contributions. It cannot currently accept contributions from an employer or a limited company, though some other providers do allow this.

-

Some members who were looking to transfer in from workplace pensions have found that fees elsewhere are still competitive, and so have not proceeded with the transfer.

It is always worth looking past the hype and knowing what to look for, and that is something we teach in the Academy. We have heard over the past week from our recent Academy graduates about how they have started to realign their retirement plans or their children's savings, putting into practice the structural changes they learned in just a few short weeks.

Article 3: What happens when a compliant stock turns non-compliant

When a company held inside an Islamic fund loses its Shariah-compliant status, it is not automatically sold straight away. To understand what actually happens, there are four things to consider: whether it is sold immediately, whether there is a holding period, what happens to any gains, and whether further purification needs to take place.

As you can imagine there are lots of rules and variables. If a business changes sector (maybe through acquisition or new business development) it can trigger immediate removal from an Islamic index, but a financial ratio breach might allow a stock to remain across multiple review cycles before it is formally removed. At the fund level, managers commonly have up to 90 days to exit. Any gains made after non-compliance is announced must be donated to charity, even if the overall investment lost money. And separately, purification applies throughout, with investors expected to donate the proportion of returns linked to any impermissible income, even from stocks that were still considered compliant.

There’s a lot more to unpack so for the full article click the link below

Final reflection

How to be popular in Islamic finance

This is an easy one. If you want to be popular in Islamic finance, talk about how bad it is. Talk about how it's words being redefined, and how it's mostly built on hidden riba.

Discussions around whether aspects of Islamic finance are halal or not can focus on specific companies, products, or even the very definition of the word 'riba'. The difficulty is that each person's argument is, in a way, built on the bias of their current role.

Take us at Nisba for example. We educate people on a halal way to invest. It's in our interest to take the opinions of scholars at face value. It's in our interest to accept current products and offerings as a genuine alternative to the traditional finance system. This gives us something worth teaching. How to use what is available today to invest in a halal way.

The reality is, we could teach people how to invest regardless of Shariah compliance, much of the process is the same. But halal investing is a niche I care about, it's how I invest, and it's what I want to teach.

I'm not a scholar. I'm a finance specialist. I can teach you how to invest, but I can't debate the opinion of a mufti. I wasn't in the room when these contracts were first drafted, when lawyers and scholars spent months building the Islamic financial system we live with today. But I am here now, and what I see is demand growing. Fintechs launching. Muslims looking for halal solutions and finding more of them than ever before. Islamic finance is standing on the shoulders of giants.

My opinion, bias acknowledged, is that the system with all its flaws will produce a better system as more people engage with it. Participation drives demand. Demand drives innovation. I think we will see stricter, more refined halal options come to market over time, and I think engaging with what exists today is what makes that possible.

Responses