It's been a tough month for commodities. Depending on the exact time you check, and how the market moves between us writing this letter and you reading it, gold is down around 10% over the past month, and silver is down 20%.

When we talk about historical returns for equities and certain commodities, we talk about 7 to 10% per year. Some people are down that entire amount, or double that amount, in just one month.

Depending on when you started investing, you could be down overall, or you could be up. If you started before September 2025, you should be up. Anytime after that, it depends. Zoom out on the charts, though, and it's quite clear that if you'd been holding either gold or silver for years, you are most certainly up, and well up.

There's a psychology that gets embedded in you from the performance of your first ever investments. We've seen it time and time again. People who start investing into individual stocks and lose money can end up staying away from investing for life.

Those who invested heavily into gold and silver after the hype of the past six months, and are now significantly down, may be put off investing into commodities ever again. On the contrary, those who are well up from their silver holdings, or sold positions when the market was high, may constantly be on the lookout for the next big slump in silver to get back in. It's not only market news and hype that drives our investment decisions, it's past experiences too.

Here's the thing though: the rules of investing don't change based on what you've personally been through. Equities and commodities remain long term investments, and that fact doesn't shift depending on whether your first experience with them was a good one or a bad one. Sometimes your experiences end up reinforcing the "true" rules of the market, like learning early to ride out volatility rather than react to it. Other times, they work against you, teaching you to fear an asset class or chase a re-entry point that may never come.

The real risk isn't the drop in gold or silver this month. It's that your past experiences, good or bad, can quietly shape how well you actually stick to your investing plan, even when you know better.

Contents:

- Competition - Win a 100g bar of Silver

- Nisba updates

- Halal funds performance

- Top savings rate

- Fear and Greed index

- Educational Focus:

- Article 1: Inheritance tax

- Article 2: Tax on Stocks and Shares ISA

- Upcoming events

- Reflection

Nisba competition: Success story

Prize: Win a 100g bar of silver!

Has Nisba played a part in your investing journey? We'd love to hear your story.

We're inviting our community to share their experience with Nisba, from where you started to where you are today. Your story could inspire others on the same path, and you'll be in with a chance to win a bar of silver.

How to enter

Submit your story in either format:

- Video: a short, informal video telling us your journey

- Written submission: text accompanied by pictures or screenshots

What we'd love to hear about

- Where you started, and where you are today

- How Nisba helped you along the way

- Any confusions or misconceptions we helped clear up

- How you used to approach investing, if at all, before finding Nisba

- How your approach has evolved based on what you've learnt

We want the full picture, so feel free to be as detailed as you like.

How to submit

Send your video or written submission to hello@nisba.co.uk by the end of July 2026 to be in with a chance of winning.

Please note

- Please remove or blur out any personal or account information (account numbers, balances, provider names, etc.) before submitting.

- By entering, you agree that your story may be featured in Nisba's marketing, including but not limited to social media posts.

Nisba updates

- We hired our first interns. Make dua’a they don’t break anything

- We delivered our 4th episode of Money Matters on Islam channel - be sure to tune in every other Tuesday at 11am (until it moves to ITV ….)

- We moved office twice in a day. Don't ask

- Ansari financial management has opened its doors to booking in initial calls- more info here

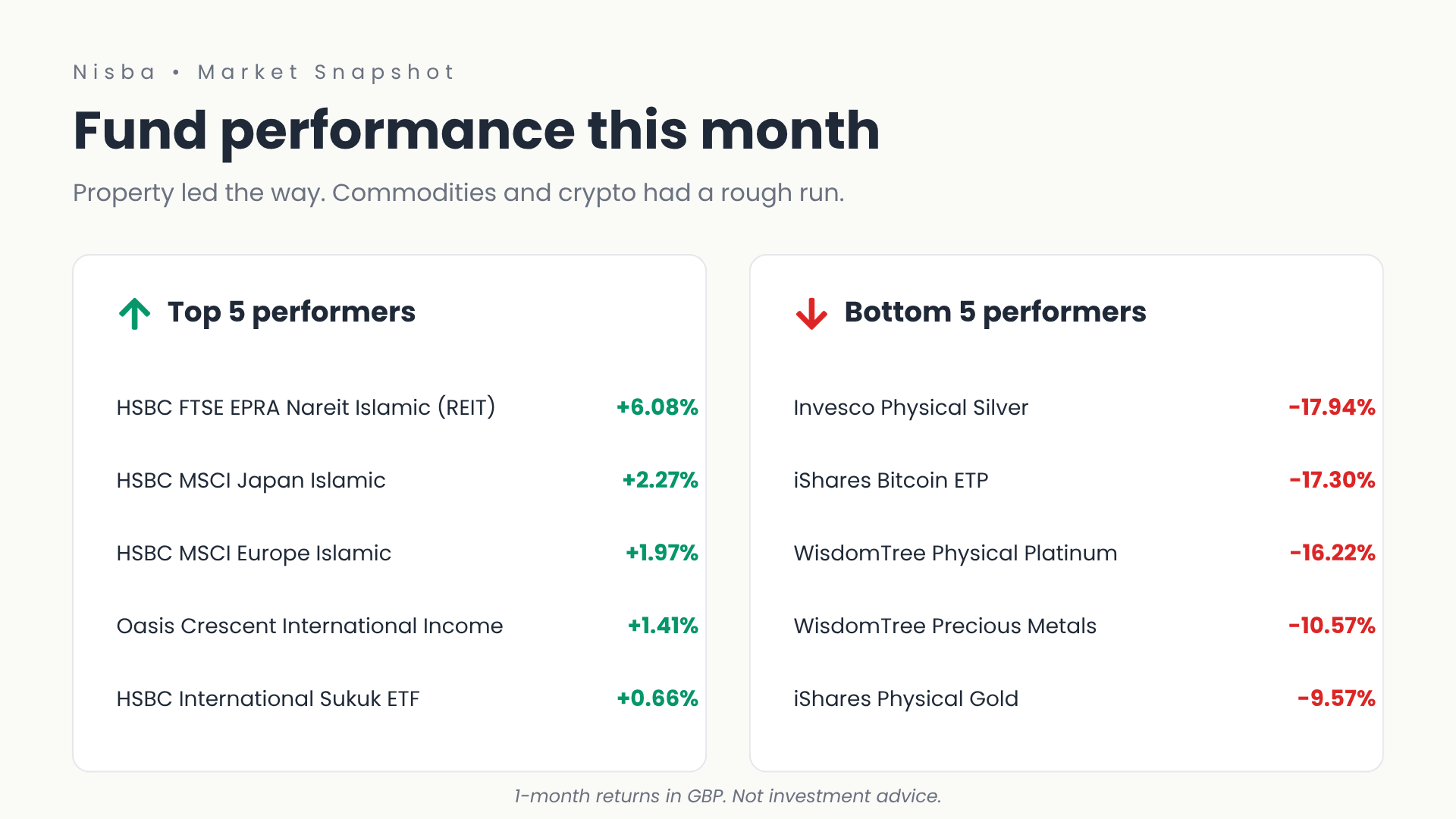

Halal fund performance (1 month)

A bit of a mixed month across the board. The top performing fund was actually a REIT, the HSBC FTSE EPRA Nareit Developed Islamic UCITS ETF, up 6.08%. Interesting to see property leading the pack rather than the usual equity suspects. Japan and Europe followed close behind on the HSBC Islamic screened side.

At the other end of the table, commodities and crypto had a rough time. Silver was down nearly 18%, Bitcoin close behind at 17%, and platinum, gold and palladium all took hits too. Emerging markets equity also gave back some of its recent gains, down 8%, which is a fair reminder that last month's high flyers can quickly become this month's laggards.

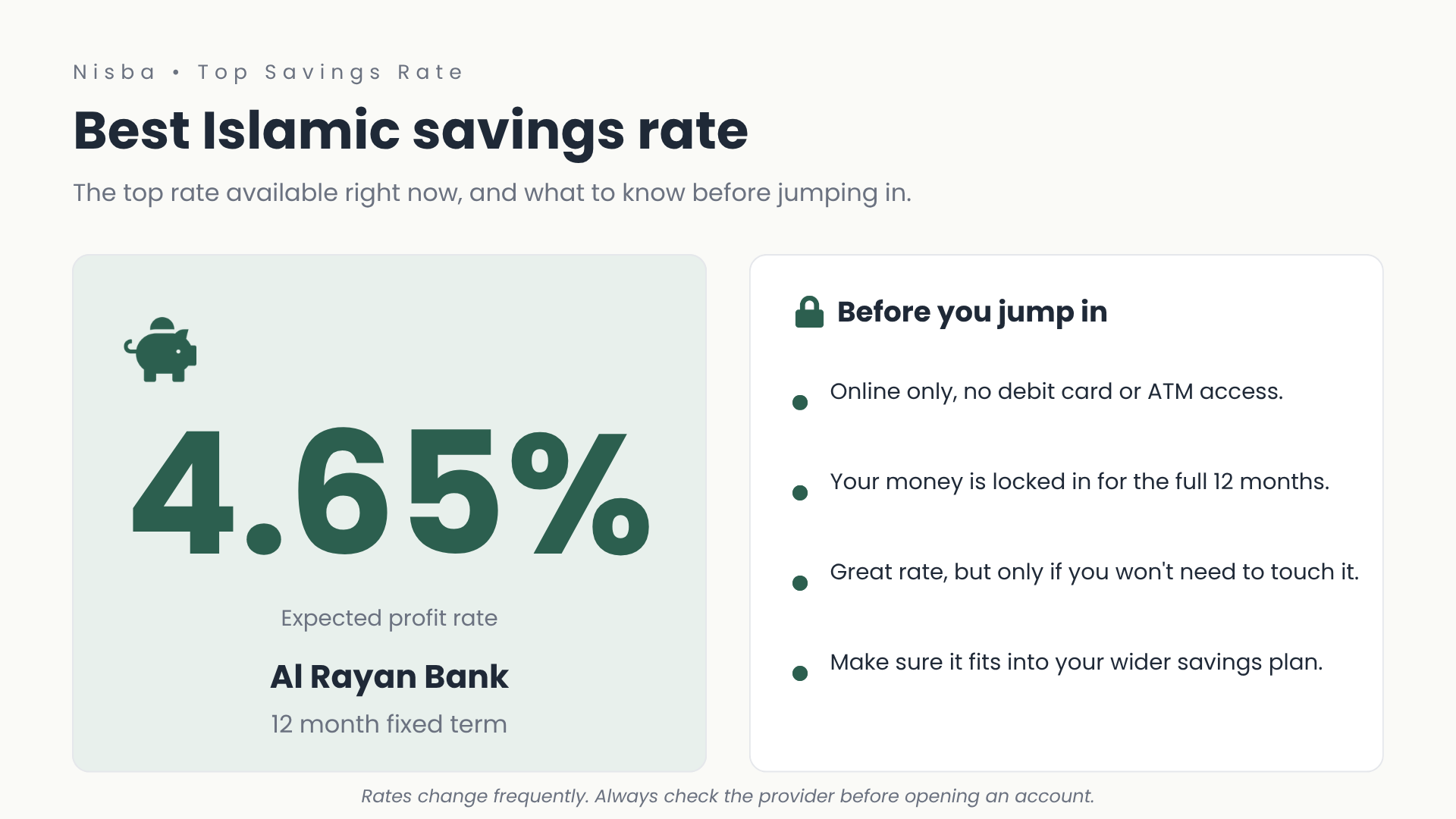

Top Islamic savings rate

On the savings side, the top rate right now is Al Rayan's 12 month fixed at 4.65%. Just remember, this one is online only, no debit or ATM card, and your money is locked in for the full 12 months. Great rate, but only if you're sure you won't need to touch it.

Fear and Greed Index

Educational focus

Article 1: The great wealth transfer, from you to the government ....

Have you heard the term ‘the great wealth transfer’ ? It refers to the fact that wealth is being transferred between generations. Most notably the great wealth transfer refers to money going from baby boomers and the silent generation to Millennials and Gen Z.

Historically speaking, one of the best ways to ensure as much money gets passed between generations without it being subject to the hefty inheritance tax is to keep it in your pension. But from the 6th April 2027, that all changes. Pensions will soon be classed as part of your estate for IHT purposes. Given the fact that the IHT allowance has remained static since 2009 and seemingly will remain in place till at least 2031. It's likely that the state will be a big beneficiary of these rules. However, IHT is the most avoidable tax.

“a voluntary levy paid by those who distrust their heirs more than they dislike the Inland Revenue”

Why? Through the use of gifts and trusts its something which can be mitigated. To know how to avoid it, and to put a plan in place. Sometimes its worth speaking to the experts.

Article 2: Are you confused about the new "22% tax on cash in ISAs" rules?

You're not alone.

Let's clear up one of the biggest financial misunderstandings doing the rounds on social media right now, the idea that the government is about to start taxing cash held inside Stocks & Shares ISAs. You may have seen videos, reels, or money gurus claiming that cash in your S&S ISA will now be taxed, or that Islamic savings profits will be hit by the new rules.

Interest is haram, but HMRC didn't get the memo

As Muslims, we already know that riba is prohibited. That's why many of us use Islamic savings accounts, halal investment platforms, or Shariah-compliant property platforms like Nester. These products generate profit, not interest, and are structured to be Shariah-compliant.

But here's the catch. For tax purposes, HMRC often labels these profits as "interest", even when they're not interest in the Islamic sense. That's caused a lot of confusion. If HMRC calls it interest, does that mean your halal savings profit is now taxable? And doesn't an ISA wrapper shield it from tax anyway?

So what actually changed?

The changes come from the Autumn Statement 2025. From 6 April 2027, for anyone under 65, the annual Cash ISA limit will fall from £20k to £12k. The Stocks & Shares ISA limit stays at £20k a year. These allowances are aggregated, so you can still put a maximum of £20k a year across your ISAs, but the cash portion is now capped at £12k.

The issue the government was trying to fix is this. Some people were using Stocks & Shares ISAs as a disguised high interest savings account, holding large amounts of cash inside them purely to earn tax free interest. Some platforms, like Trading 212, were paying pretty attractive rates on any uninvested cash sitting in a S&S ISA. So in theory, someone could park £20k in there and quietly collect interest without ever really investing.

The Treasury didn't love that, so they introduced rules to stop it.

Here's the important part

The rules target interest bearing cash deliberately held inside a Stocks & Shares ISA. They do not tax your investments. They do not tax your cash in a Cash ISA. And they do not tax your halal savings profits outside an ISA any differently than they do today. This is HMRC closing a loophole, not creating a new tax.

Does this affect halal savings profits?

Short answer, no. Not in the way people fear.

Halal savings accounts sit outside the ISA system entirely. So even though HMRC may classify their profit as interest for tax purposes, they're not part of these circumvention rules. Even halal savings accounts inside a Cash ISA are unaffected.

What about platforms like Nester that pay profit on investments?

Also no. You receive profit on your actual investment, not on dormant uninvested cash. The circumvention rules only apply to cash held inside a Stocks & Shares ISA or Innovative Finance ISA, earning interest, where the ISA is essentially being used as a tax free savings account rather than an investment account.

Upcoming Events

- Is your pension halal

- Intro to halal investing

- Angel investing for muslims

Final reflection

I very often think business can be a lot like football.

Last week Senegal were winning 2-0 against Belgium. I turned the TV off and headed to the mosque for isha.

Around the 80th minute, you can probably imagine many Belgians were thinking, this is it, we're done.

To be honest, I have thoughts like that sometimes when it comes to certain parts of this business. Every day people reach out asking for help with their investments. And I know the book we have written and the Academy would solve pretty much everything they're asking about. But somehow it still doesn't quite land.

The education we offer is genuinely unrivalled, that part I'm sure of. It's just proving harder than expected to get people to see the value of it before they need it.

Then I came out of the mosque, checked my phone, and saw Belgium had pulled two back and won it in extra time.

Down 2-0 with ten minutes to go, and they still turned it around.

These things take time I guess and can snowball very quickly. So we go again.

See you in a few weeks inshaAllah.

Interested in joining our WhatsApp group

If you are interested in financial advice, please fill out this form

I'm interested in getting financial advice

Responses