Can’t believe it took us this long to pinpoint what we are teaching at Nisba. Funnily enough we didn’t even figure it out ourselves. A client kindly told us.

I’ve always found the concept of investing quite easy. You can listen to a 1 minute video and they’ll say “buy this equity fund, stick it in an ISA” that’s how you start investing. Sure enough that’s how many people start, find an Islamic equity fund, copy a pie on Trading 212. Good. To. Go.

So what’s missing? Why does it take us a month to teach that? We’ve found that people don’t know when to sell (because they don’t have a plan). Also they get freaked out when the market dips (again, no plan). They pick the wrong account type for their goal. They invest the wrong amount. There's a complete mismatch between what they are investing in and what they are investing for. There's no payday routine. A lack of understanding leads to the majority of their time comparing one islamic equity fund to another.

I don’t know how many times I’ve said it this year. Here we go again:

“The specific choice of equity fund you choose is one of the least important decisions you’ll make when investing.”

And now we know, we don’t teach ‘investing’. We teach a halal wealth management system which revolves around you, whatever stage you are at. Sometimes it takes a minute for the penny to drop, it took us months. But now we know the value of what we teach.

Contents

- Competition - 14 days left to win a 100g bar of Silver

- Nisba updates

- Halal funds performance

- Top savings rate

- Fear and Greed index

- Educational Focus:

- Article 1: 6 exams to understand pensions

- Article 2: Costly mistakes to avoid

- Upcoming events

- We need your help

- Reflection

Nisba competition - 14 days to go

Win a 100g bar of silver. Share a short story (not AI generated please) about how Nisba has helped your investing journey. It could be a quick video or a written submission with a few screenshots.

Send it to hello@nisba.co.uk by the end of July 2026. Please blur any personal or account info before submitting, and note that by entering you're happy for us to feature your story in Nisba's marketing.

Thouands of you have reached out to say how we have helped, we would love to share some of these stories and encourage others to maybe start.

Nisba updates

- Our latest podcast with a muslim fund manager manging more than $500m is now live on YouTube

- We are hosting an in person Introduction to Halal Investing - come learn and say salaam at the same time - Monday 27th July

- We have teamed up with Family Break, we are planning to deliver a seminar for them and managed to secure a discount for anyone planning to go who uses this code (NSB10)- More info here

- Our next academy starts in August. If you are looking for a full halal money system from budgeting, payday routines, to tax effecient investing and managing wealth for the future - see here for more info

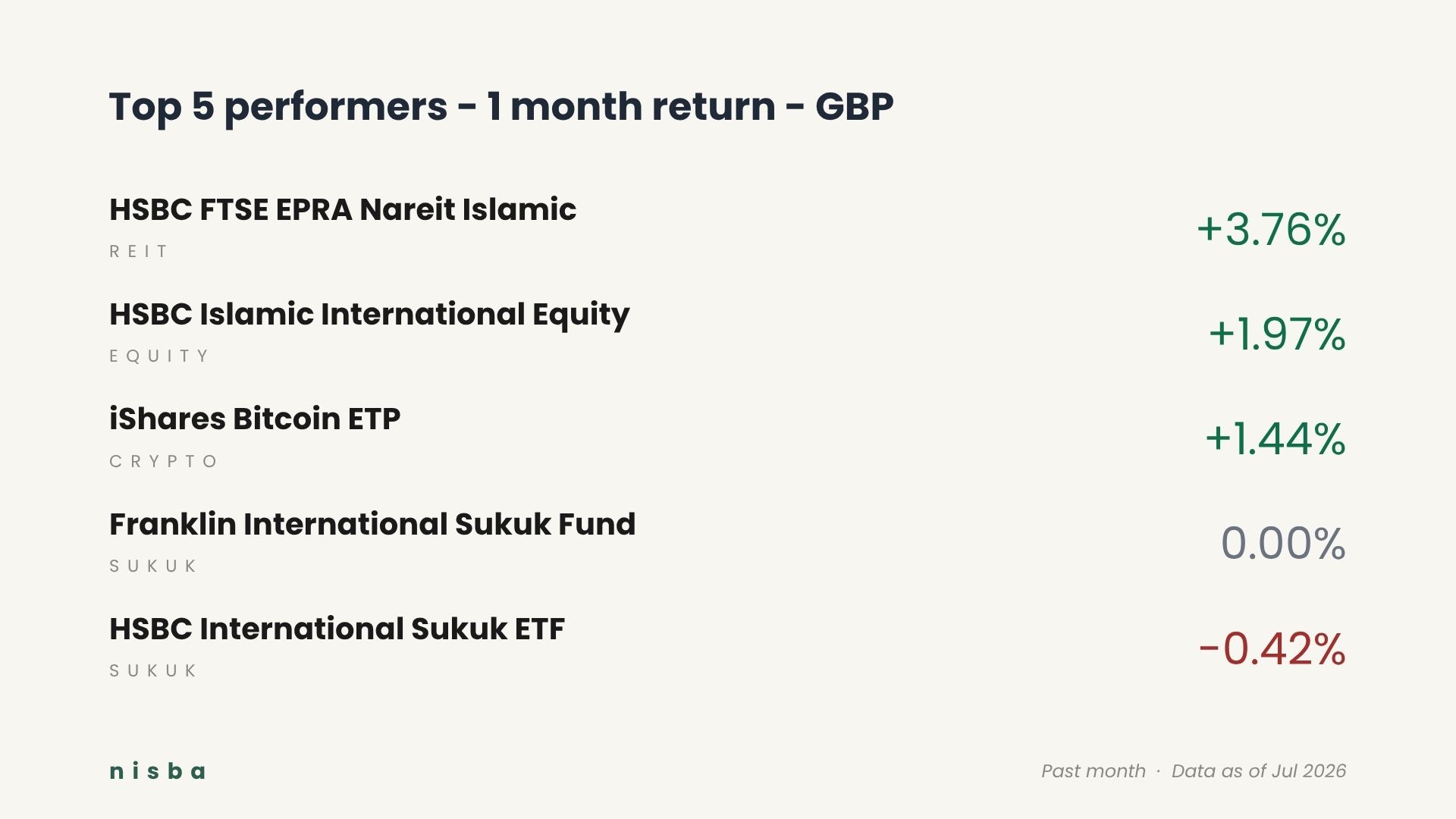

Halal fund performance - 1 month

Rough month for commodities, with silver, precious metals, platinum and palladium all taking heavy hits. Emerging markets also gave back some ground after a strong run earlier in the year. On the flip side, REITs led the pack this month, though of course past performance is never a guide for what comes next.

What do you think we'll see next month?

For a full list of shariah compliant funds - www.nisba.co.uk/funds

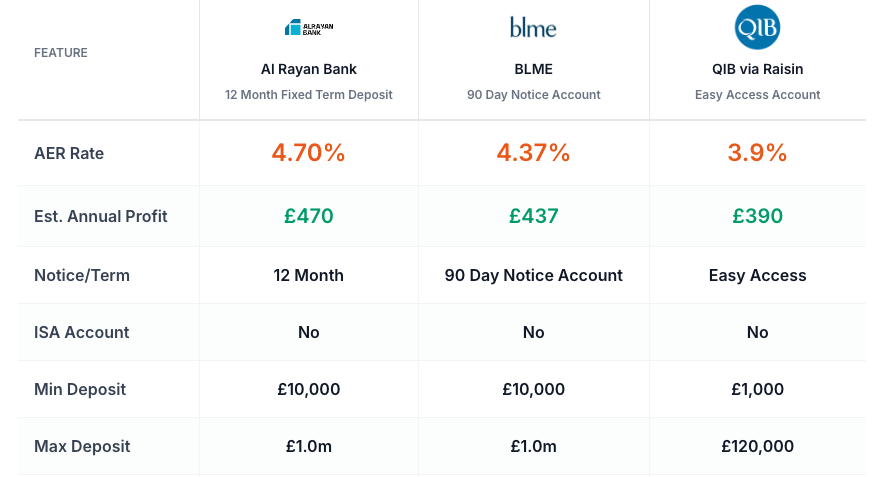

Top savings rate

Here are the top rates across the three different account types for shariah compliant savings accounts. Interestingly, we see another rise in the fixed term accounts.

For a full list of savings accounts - www.nisba.co.uk/savings-accounts

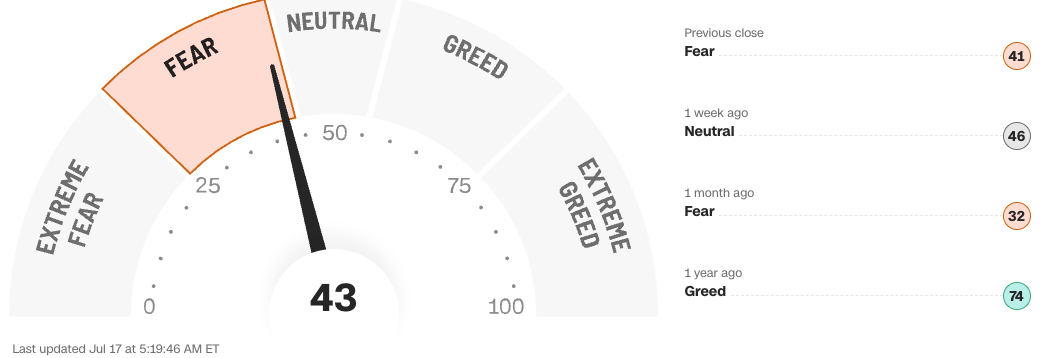

Fear and Greed

What is it: The Fear and Greed Index is a simple gauge of how the market is feeling right now, running from 0 (Extreme Fear) to 100 (Extreme Greed). It's a useful gut check on whether decisions are being driven by logic or emotion.

Commentary: The index is sitting at 43, in Fear territory. Not surprising given the week we've had, with a sharp selloff in chipmakers dragging down Wall Street as investors question whether the massive AI investments can justify current valuations, and renewed geopolitical tensions after Trump announced he was reinstating a blockade on Iranian shipping through the Strait of Hormuz, sending oil prices higher. A year ago the index sat at 74, firmly in Greed, so sentiment has cooled considerably. Worth remembering though that Fear is often when the best long term opportunities quietly appear.

Educational content

Article 1: 6 exams to understand a simple term

I (Ahmad) started my exams to be a financial advisor in 2021, a couple hiccups because of covid later, I finished my exams in 2023. I did it to understand my pension. Yes, I trained, and did 6 exams to qualify as a financial advisor, to understand my own pension. By the end, I still didn't understand my pension.

Too many acronyms, MPAA, UFPLS, PCLS, AVCs, pff. I think someone is trolling the public with pensions to make them perhaps a bit more complicated than they need to be.

Alas, we are bound by the system and we live in it. I only really started understanding pensions when I had to advise people on them. Hours of research each time to understand what’s going on. Forced to break things down. Only when I could explain pensions to others did I realise I had cracked it myself.

Funny, I thought to google which country has the most complicated pension system:

“The United Kingdom is widely cited by global economists, pensions commissions, and the media as having arguably the most complicated and complex pension system in the world”

Maybe my google is biased. The sad thing is, now that I understand pensions (quite well), I can't quite remember what part I was confused about. If only I did, then I would have spent the past few paragraphs demystifying that specific part. Instead I just spoke about how confusing they are.

To help you with halal pensions, we did an online webinar on halal pensions, to watch it free, click here.

Passcode: St0G#=9.

Article 2: When rumours cost you money: A lesson in retirement panic

If you've been reading the Nisba Newsletter for a while, you'll remember our warnings about hype. Don't jump on bandwagons, don't act on rumours, and always wait for official confirmation. New research from Quilter shows exactly why that advice matters, especially when it comes to your pension.

What actually happened

Quilter surveyed 5,000 UK retirees and found that 57% withdrew tax free cash from their pension pots before last year's Budget. Of those, 41% did it because they feared the rules were about to change. Social media was buzzing with speculation that the 25% tax free lump sum might be cut. No official announcement. No confirmed policy. Just noise.

The result? 61% of those who withdrew early now regret it. That's a lot of people who acted out of fear rather than need.

How the rumour mill did the damage

In the run up to the Budget, silence from the Treasury was interpreted as bad news. Retirees assumed something big was coming and rushed to lock in the existing rules. But no formal proposal to change the tax free lump sum was ever put forward. People simply stated to act on speculation.

Quilter found the withdrawn money was mostly used for home improvements, healthcare costs, gifting to grandchildren, or day to day living. Some of these were necessary, but many retirees admitted they wouldn't have touched their pension at all if they hadn't been spooked.

Why this matters for Muslim savers

For Muslims, retirement planning is about amanah, responsibility, and making choices that align with our values. Rushed decisions driven by rumour can lead to unnecessary tax bills and long term regret. This is why the Nisba Academy focuses so heavily on critical thinking around financial news, and why our partner Ansari Financial Planning emphasises regulated, personalised advice. AI tools, influencers, and money gurus can't replace proper guidance, especially when the stakes are this high.

The bigger lesson

Quilter's head of retirement policy summed it up nicely, retirees acted out of fear, not need. And that fear came from rumour, not reality.

It's the same pattern we've flagged before, whether it's the SpaceX IPO hype, crypto trends, or pension rumours. Acting before the facts are confirmed usually isn't in your best interest.

Upcoming events

Sunday 26th July - Intro to halal investing (online)

Monday 27th July - Intro to halal investing but in person (North London)

Platform updates

There are two new sukuk funds

Interestingly, there are 2 Franklin sukuk funds which are hedged on AJBELL the S class with fees of 0.45% and the W class with fees of 0.9%

Unfortunately, the S class is restricted and I called AJBELL to ask if I can buy it and they asked how much I'm looking to invest so they can contact Franklin temptaton…. Seemingly not gonna happen with my minor funds.

The sukuk space is getting more interesting with the 2 relatively new sukuk funds being pushed out on platforms namely

1) the Franklin ultra short sukuk fund (currency hedged, fees of 0.25%)

2) DWS sukuk fund

The ultra short sukuk fund is VERY interesting. The DWS fund is just another standard one and I wouldn’t really understand why someone would opt for the DWS fund over the other options

The Franklin ultra short duration fund invests into sukuk which are ultra short duration. In other words the fund price isn’t affected my by interest rate moves.

Movement in interest rates is what caused sukuk and bond funds to have one of their worst years ever back in 21/22.

Fees on this fund are 0.25% making it one of their cheapest shariah-compliant funds you can invest in.

There’s also a new DWS Salam sukuk ETF. There is nothing interesting about this sukuk fund I think.

The unfortunate thing with ultra short duration sukuk, is they have a lower return, but that should make sense, as they are less risky.

HalalScreener

HalalScreener is going from strength to strength. More rigorous BDS checks underway, more user feedback and more users adopting this tool. If you are interested to learn more investing in a shariah compliant and boycott friendly way - see here.

We need your help

We run a small academy cohort every month, and every time, everyone is more than satisfied. We are trying to work out why more people arent signing up. Can you answer just one question for us, should take 60 seconds

If you are part of the Whatsapp group and have already answered, no need to answer again

Final reflection

A worthy investment that makes nothing?

You have £100,000 in an Islamic savings account that earns 4%, after 1 year you make £4,000. On the £100,000 - £2,500 of Zakat is due. Tax will likely be due too, either at 20% with a £1,000 allowance or 40% with a £500 allowance or 45% with a 0 allowance. Let's assume you are a higher rate tax payer, so 40% tax is due on £3500 (£4000-£500 allowance), that's £1,400 in tax to pay.

Overall, after Zakat and Tax you are left with £100. A net return of 0.1%. We haven't even factored in inflation, which would leave you with a negative ‘real’ return. Not ideal, but still better than doing nothing with the money and paying Zakat on it anyway.

So what’s the point of this little outro piece? For me, it’s that there’s more to investing than meets the eye. Sometimes a little extra digging is needed to find out what’s really going on.

P.s - If you are interested in regulated financial advice, fill in this form and Ahmad will be in touch via Ansari Financial Planning.

Responses