Islamic Savings Accounts in the UK: What Every Muslim Should Know

Jun 02, 2026

The UK offers more choice for halal savings than almost anywhere outside the Muslim world. Here is what the market looks like, how profit rates work, and why every Muslim should consider having one.

If you are a Muslim living in the UK, you are in a surprisingly privileged position when it comes to Shariah-compliant savings. While Muslims in most non-Islamic countries have little to no access to halal savings products, the UK has developed one of the most competitive Islamic retail banking markets in the world outside of the Muslim world.

More choice than almost anywhere else

Islamic banking in the UK has grown significantly over the past two decades. Today, UK residents have access to a range of dedicated Islamic banks and financial institutions offering Shariah-compliant savings products: Al Rayan Bank, BLME (Bank of London and The Middle East), Gatehouse Bank, QIB UK, Kuwait Finance House, and Habib Bank Zurich all offer competitive halal savings accounts, fixed-term deposits, and notice accounts.

Compare this to France, Germany, or the United States, where dedicated Islamic retail banking is either absent or extremely limited, and you start to appreciate the depth of the UK market. This is partly a result of the UK government's long-standing commitment to making London a global hub for Islamic finance, and partly due to the size and economic profile of the UK's Muslim population.

Profit rates: not guaranteed, but consistently paid

One of the most important things to understand about Islamic savings accounts is that the returns are structured differently from conventional interest. Banks advertise an "expected profit rate" rather than a guaranteed interest rate. This distinction matters in Shariah law: money cannot earn a return simply by virtue of existing, it must be put to work in a real economic activity.

In practice, Islamic banks use your deposits to finance Shariah-compliant activities: home purchase plans, business financing, and property development. The profits generated from these activities are then shared with depositors according to the agreed profit-sharing ratio.

Important note: While profit rates are not contractually guaranteed, UK Islamic banks have consistently paid their advertised expected profit rates. No UK Islamic bank has ever failed to pay savers their expected return. This track record gives depositors a high degree of practical confidence, even if the legal structure is different from conventional interest.

Islamic banks typically hold a portion of profits in a reserve, sometimes called a Profit Equalisation Reserve, which can be drawn upon to supplement returns during lower-profit periods. This smoothing mechanism means customers experience relatively stable rates even as underlying economic conditions shift.

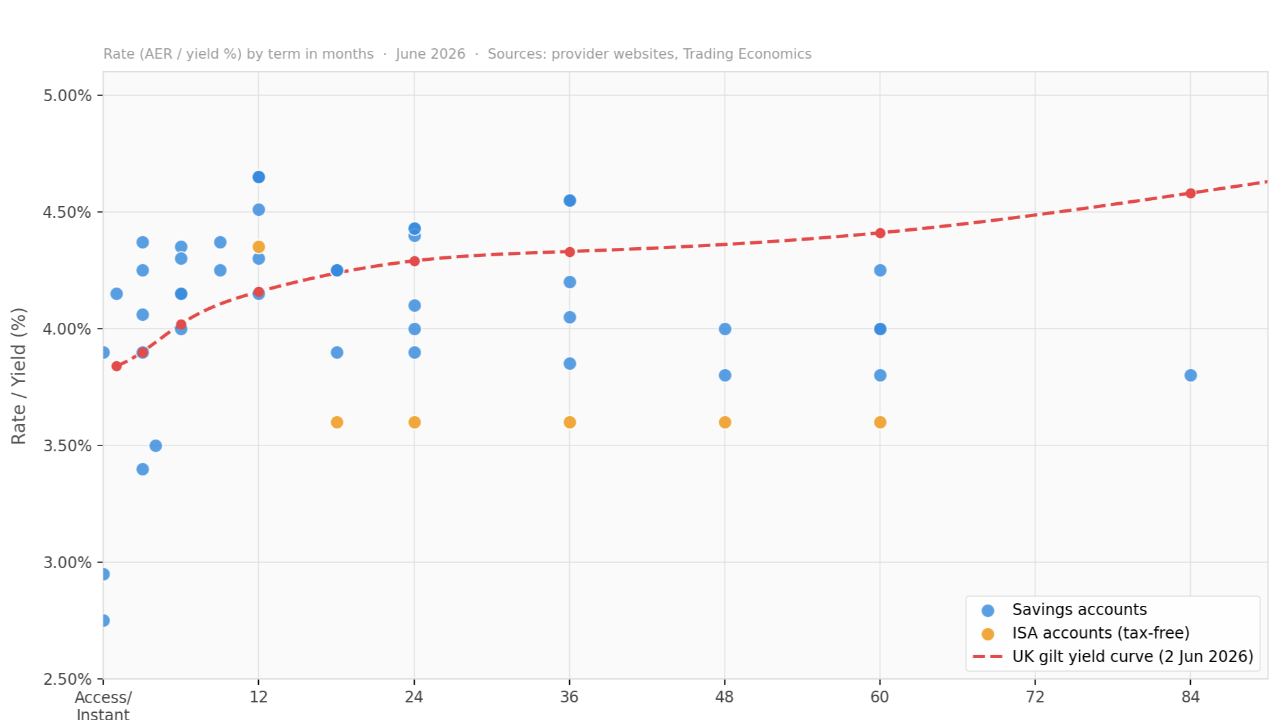

How profit rates are set: the gilt connection

Here is something that surprises many people: Islamic bank profit rates broadly track the UK gilt yield curve, even though they have nothing to do with interest.

This is not a contradiction. Gilt yields reflect the broader cost of money in the economy, they move with inflation expectations, Bank of England policy, and global capital flows. Islamic banks operate in the same economy and compete for the same pool of savers. When the risk-free rate (gilts) rises, savers expect more from everywhere, including their Islamic accounts. When gilt yields fall, profit rates tend to follow.

The chart shows the current UK gilt yield curve alongside every available Islamic savings product, plotted by term and rate. The pattern is clear: profit rates broadly follow the shape of the gilt curve.

It is worth being clear about what this connection to gilt yields does and does not mean. The fact that profit rates move in line with broader market rates is simply a reflection of economic reality. Islamic banks cannot price in a vacuum. But the underlying mechanism is entirely different. There is no loan, no interest, no predetermined return. The bank deploys your money into halal assets, earns a profit, and shares it with you. The number may look similar to an interest rate; the structure is fundamentally different.

The ISA question: only one provider, with an interesting anomaly

Currently, Gatehouse Bank is the only Islamic bank in the UK offering a Shariah-compliant Cash ISA. For Muslim savers who want to shelter their savings returns from income tax, the options are therefore limited to a single provider.

Gatehouse offers Cash ISAs at fixed terms from 1 to 5 years. There is, however, an interesting quirk in their pricing. At the 1-year term, the Cash ISA pays 4.35%, which is actually higher than their non-ISA 1-year Woodland Saver at 4.15%. Normally you would expect the ISA to pay slightly less, since the tax benefit itself has value. The most likely explanation is competitive ISA season pricing: banks often push ISA rates higher around the April tax year end to capture annual ISA allowance inflows, and Gatehouse appears to have retained that pricing premium.

The practical upshot: if you have ISA allowance remaining and are considering Gatehouse, the 1-year Cash ISA is currently the better deal even before the tax benefit is factored in.

FSCS protection: your money is safe

All of the Islamic banks listed here, Al Rayan, BLME, Gatehouse, QIB, Kuwait Finance House, and Habib Bank Zurich, are covered by the Financial Services Compensation Scheme (FSCS). This means your deposits are protected up to £120,000 per person, per banking licence. If an Islamic bank were to fail, your savings up to that limit would be fully protected by the UK government scheme, exactly as with any conventional bank.

Every Muslim should consider having one

For a Muslim who keeps money in a conventional savings account, every penny of interest earned is potentially impermissible. Many Muslims are aware of this but have not acted, either because they assume Islamic savings rates are lower, or because they believe the process of switching is complicated.

Neither assumption holds up in 2026. As the chart above shows, the best Islamic savings rates are genuinely competitive, in some cases beating conventional equivalents and even gilt yields at the 12-month mark. Opening an account with Al Rayan, BLME, or Gatehouse is no more complex than opening any other savings account, and several providers are available through the Raisin UK platform, making comparisons and applications straightforward.

There is no good reason for a Muslim in the UK to be keeping their savings in an interest-bearing account. The halal alternatives are there, they are competitive, they are FSCS protected, and they are easier to access than at any point in history.

For an up-to-date list of Islamic savings account rates, visit nisba.co.uk/savings-accounts.

Learn more about Halal Investing

Stay up to date with halal investing

Join our mailing list for the latest insights, updates, and opportunities from Nisba.

We respect your privacy, no spam, ever.