When the ceasefire was announced, markets reacted strongly. It was a very positive day, I saw some Islamic emerging market equity funds up close to 10%. In fact, we’re already almost back to where we were before the conflict escalated.

I know some people who sold during the downturn out of fear. Maybe they didn’t have a clear plan in place. Decisions driven by headlines and global events can sometimes work in your favour, but more often than not, they just add stress and inconsistency to your investing.

I don’t think this is the end of the Iran situation. But I came across a quote recently that captures where we are quite well: “This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

If anything, this is a reminder of how quickly markets can move, and how difficult it is to time them. If there was ever a time to be fearful about taking on too much risk for short term goals, that time might be now.

Contents

- Nisba Updates

- Halal Fund Performance

- Top Halal Savings Rates

- Fear & Greed Index

- Platform Updates: AlRayan, Cur8, HSBC, Kestrl, Gold, RFF

- Islamic Reflection: It exists before you are born and after you die

- Competiton Time

- Educational Focus 1: You can open so many ISAs in a single year, doesn’t mean you should

- Educational Focus 2: Pension news

- When the smartest people in finance nearly broke the system

- “This Is More Halal Than That”: an opinion piece by Ahmad

-

Final Reflection

Nisba Updates

The team at Nisba has been working on something new behind the scenes. We’re building a halal wealth tracker to make it easier for Muslims to manage and grow their money in a Shariah-compliant way. This week we launched the beta with our first group of users. Exciting times ahead, inshaAllah.

We’ve also added extra value to the Nisba Academy. To be honest, we didn’t include all of this for previous attendees, but given we’ve consistently received 5/5 reviews, we’re hoping this takes things to another level. You can check it out at nisba.co.uk/academy.

We’re now officially looking to hire a summer intern. Ideally someone at university with an interest in Islamic finance. We have a small office in North London which comfortably fits two people, three at a push, and we’d like the intern to work with us there three to four days a week. To apply, send your CV along with one thing you think Nisba can improve and how you would improve it. That idea might just become your project for the summer. You do not need a background in finance, any skill that is valuable to a business will do (anything really). Send it through to hello@nisba.co.uk

The first batch of the Nisba Playbook is almost sold out, with only a few copies remaining. I don’t expect it to become a collector’s item in ten years, but you never know. If you want one of the last physical copies, mainly because you want a solid reference for halal investing in the UK, you can find it at nisba.co.uk/playbook.

In case you missed it, we recently launched the Nisba Halal Screener. It connects to Trading 212 and builds a custom halal equity pie based on the S&P 500. You can try it here: tools.nisba.co.uk/nisba-halal-screener.

We also released a video on our first Nisba competition where we gave away 100g of silver. Participants picked a stock and we invested £20,000 across all selections for the month of January. Where did it end up by the end of the month? Watch the video to find out: https://www.youtube.com/watch?v=N1Xfk7XvkOs

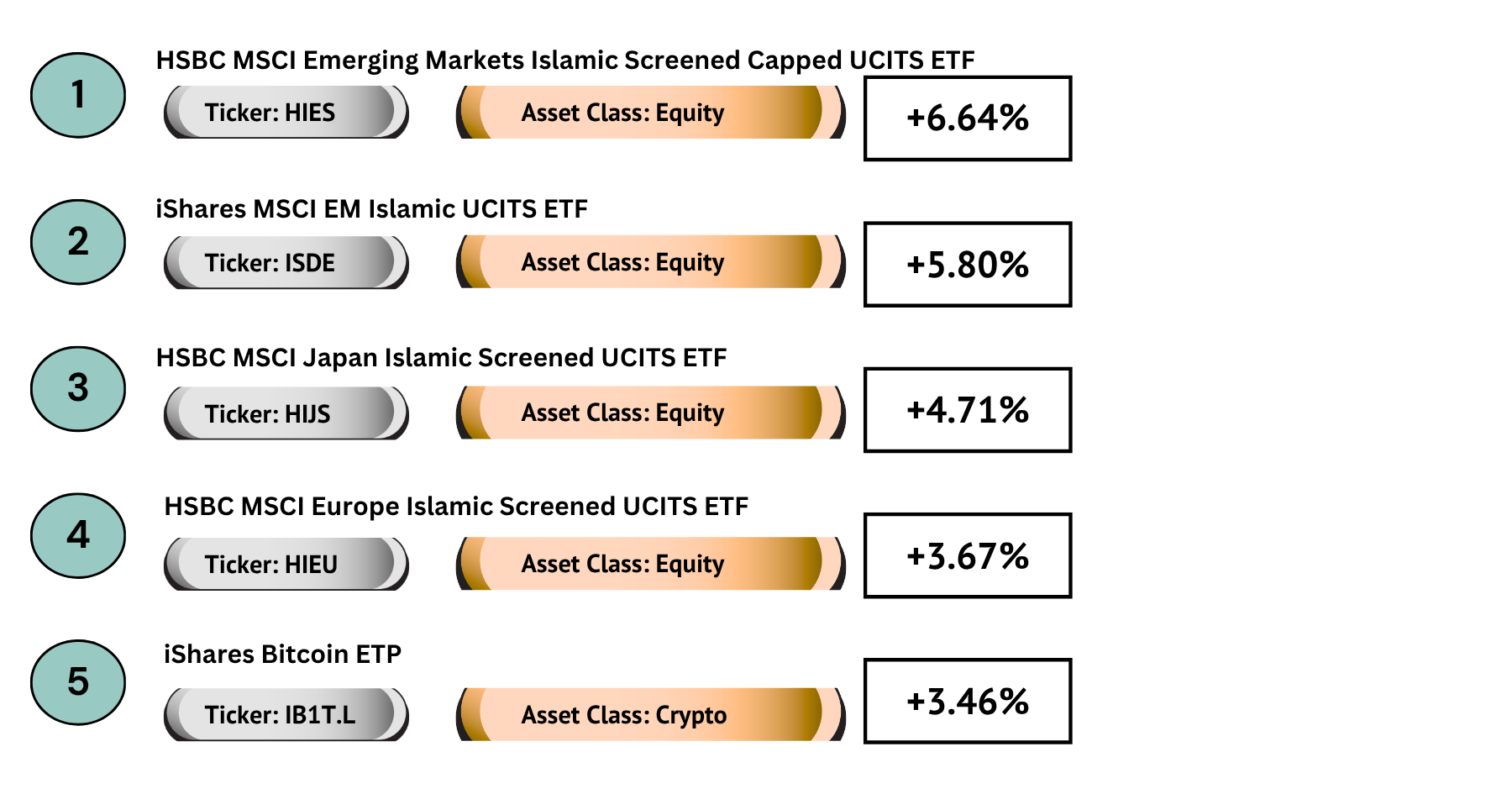

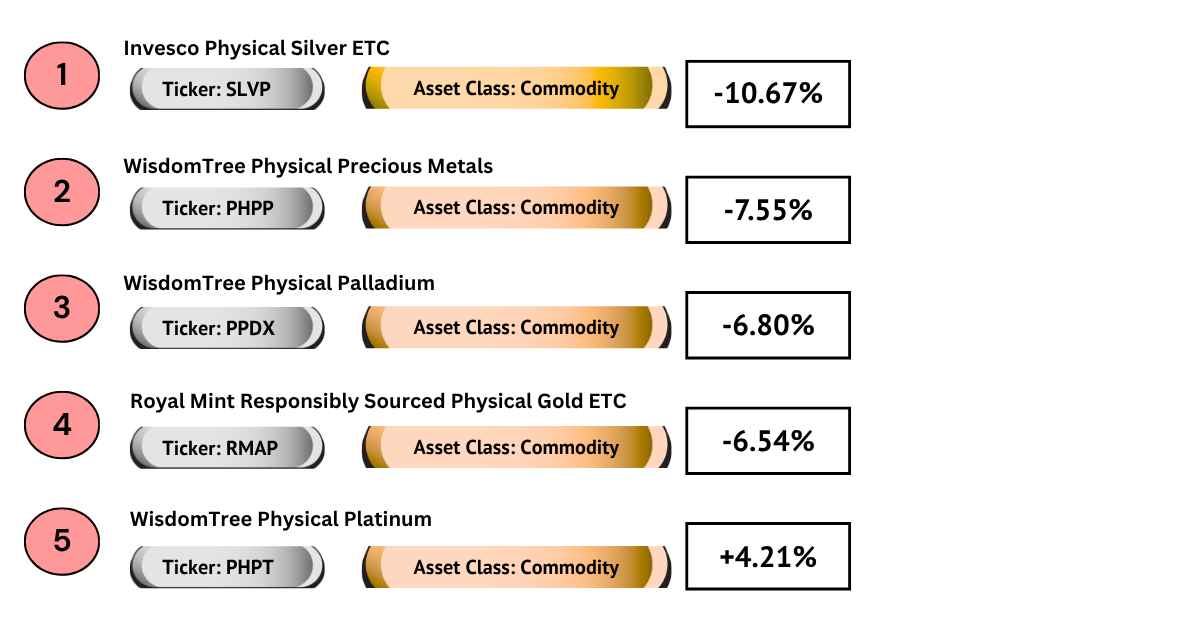

Halal Fund Performance

Top 5 Best 1-Month Performers

Bottom 5 Worst 1-Month Performers

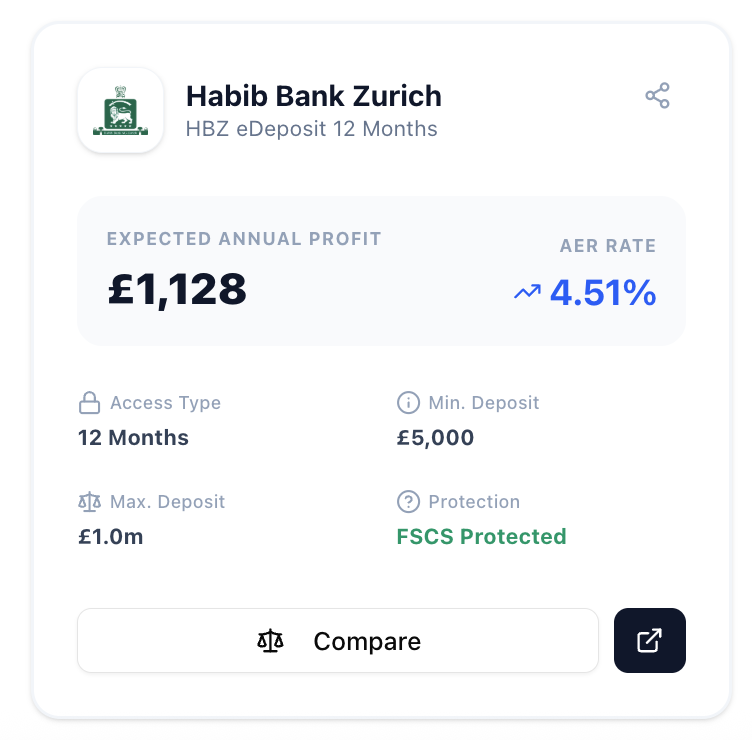

Top Savings Rate

Two weeks ago, we saw top rates around 4.34%. Today, that’s moved up to around 4.51%.

It feels like a bit of a mixed bag right now with Islamic savings accounts. Some providers are increasing their expected profit rates, while others are starting to bring them down.

It’s a reminder that even in the savings space, things are constantly moving, and it’s worth keeping an eye on where you’re holding your cash.

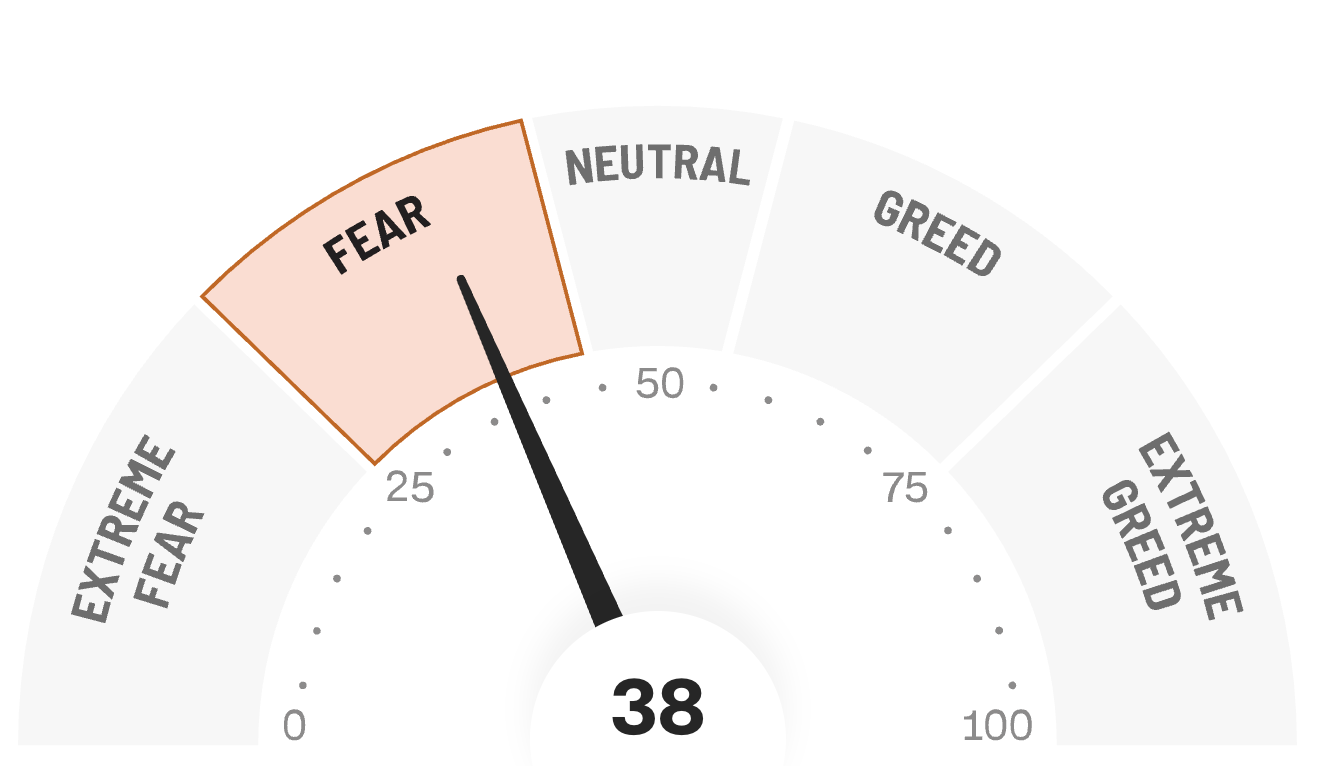

Fear and Greed Index

What is it? The Fear & Greed Index is like a mood tracker for the stock market. It looks at 7 different signals to give the market a score from 0 to 100, where 0 means investors are really scared, and 100 means everyone is feeling super confident and buying everything in sight.

Commentary: Currently the index is sitting at 38 - Fear. This is an improvement from last week when we were at 18, which was Extreme Fear.

This shift could partly be linked to recent geopolitical developments, including the temporary ceasefire between the US and Iran, which has slightly eased market tensions, even if the situation remains fragile.

So while the mood is still cautious, it has started to recover. For patient long-term investors, moments like these can still present opportunities if you stay disciplined and stick to your plan.

Platform Updates

Trading 212

This is a big one. Trading 212 has now introduced a SIPP. Previously, many people were using Trading 212 for their Stocks & Shares ISA and then having to use another platform like AJ Bell for their pension.

We haven’t used it ourselves yet, but from initial research:

-

Fees: No platform fees, which is a huge win compared to many traditional providers. FX fees still apply for non-GBP investments.

-

Investments: Same range as the ISA, including ETFs and individual stocks. This is especially powerful given the solid range of Islamic ETFs already available on Trading 212.

-

Transfers: Pension transfers should be possible, depending on your current provider. Always check for exit fees.

-

Tax benefits: Standard SIPP rules apply. £80 becomes £100 with basic rate tax relief.

-

Access: Locked until pension age (currently 55, rising to 57).

It’s also currently in beta, so not available to everyone yet and features may change.

Overall, this has the potential to massively simplify things for a lot of people who want everything in one place. Definitely one to watch.

Cur8 Capital

The team at Cur8 Capital have been sending out a few messages recently about closing allocations to their EIS venture capital fund. It looks like they’re making a final push for investors before the window closes on 14th April.

They’ve also mentioned some positive developments across the underlying investments over the past six months. Encouraging to hear, although I haven’t seen any reflection of that yet in my own investment.

That said, it’s probably not surprising. Early-stage companies are difficult to value, and updates tend to lag until there’s something more concrete to anchor valuations to. It may simply be that the app hasn’t been updated yet, or that they’re waiting for clearer data before making any adjustments.

Either way, it’s a good reminder of what you’re signing up for with venture investing. Progress can be happening in the background long before it shows up in your portfolio.

AlRayan Bank

AlRayan Bank is tightening the criteria for opening and maintaining savings accounts directly with them.

The minimum balance is increasing from £5,000 to £10,000, and accounts may now be closed if the balance falls below that level. They’ve also extended the notice period for closing a current account opened after 28 April 2026 from 60 days to 90 days.

Another notable change is their participation in the Dormant Assets Scheme. This means that if an account remains inactive for 15 years or more, funds may be transferred out of the bank.

From what I understand, these changes may not apply if you’re accessing Al Rayan products through platforms like Raisin or AJ Bell, which offer savings marketplaces.

Overall, it looks like a move towards targeting larger balances and longer-term customers. Definitely worth being aware of if you’re using, or planning to use, AlRayan for your savings.

HSBC

A new potential addition to the halal investing universe is on the horizon.

HSBC is preparing to launch a Shariah-compliant global infrastructure equity strategy, focusing on sectors like utilities, transport, energy, and telecoms. The aim is to provide a more defensive, income-generating building block within a portfolio, with lower volatility and more resilient cashflows compared to traditional equities.

What’s interesting here is the positioning: many halal portfolios today are heavily concentrated in tech and growth stocks, so infrastructure could offer diversification and balance.

It’s still early (and not yet available to retail investors), but it’s a positive sign that the range of halal investment options continues to expand.

Gold

Maybe we’re stretching a bit with this one, but the team at PAMP have released an Eid Mubarak gold bar.

As you’d expect, it comes at a premium compared to buying gold through funds or standard bullion. You’re paying for the design and collectability as much as the gold itself.

That said, some people will absolutely love it. As a gift or something a bit different, it’s a nice touch. Just don’t confuse it with the most efficient way to invest in gold.

Kestrl

Kestrl is picking up serious momentum.

They’ve announced they’re nearing £500k in deposits as part of their £1m milestone, which, if reached, unlocks the next phase of their roadmap, including ISAs, financing products, and more via their Maybank London partnership.

Why this matters: one of the biggest gaps in the UK right now is everyday Islamic banking. If platforms like Kestrl can reach scale, it opens the door to more practical, accessible halal financial products beyond just investing.

Still early days, but definitely one to keep an eye on.

Riba Free Foundation (RFF)

RFF is a UK non-profit that helps remove riba via donations.

They use these funds to educate communities on the harms of riba and promote ethical, interest-free financial alternatives.

They’ve also launched a Riba-Free Product Directory to make it easier to find trusted, Shariah-compliant financial services.

Islamic Reflection

There’s something that was here before you were born, and will be here long after you’re gone. Money.

In Islam, we’re constantly reminded that we don’t truly own it. We’re custodians of it. It’s a means through which we are tested. How we earn it. How we save it. How we spend it. How we give it.

Interestingly, I heard a similar idea from a non-Muslim for the first time this week. The conclusion, though, was very different. The idea was that money is temporary, so you might as well just enjoy it.

Islam gives that same premise a completely different direction. It’s temporary, yes. But that’s exactly why it matters how you use it.

Rumour has it I’m giving a talk soon for the KCL ISOC Alumni on building a stronger Muslim community. My initial thought was simple. More money equals more power, which should lead to a stronger community.

But when you look around, there are individuals and even entire nations with wealth, yet the strength we’re looking for isn’t there. So the answer isn’t money on its own. It’s having the right foundation in place. So that when money or influence comes, it’s used correctly. With purpose, responsibility, and direction.

Money doesn’t build a strong community by itself. People with the right principles do.

Competition Time

We’ve got an exciting competition in collaboration with the launch of Time Hoppers: The Silk Road, the first ever Muslim animated film to receive a nationwide UK cinema release.

You could win up to 6 cinema tickets for a screening near you, a Nisba hoodie, and a Nisba Playbook.

To enter:

-

Like our Instagram post

-

Follow both accounts

-

Comment “Time Hoppers”

Keep an eye on Instagram over the coming days for the post.

Good luck 👀

Educational Focus

You can open multiple ISAs in a year… doesn’t mean you should

With the recent ISA rule changes, you can now open and pay into multiple ISAs of the same type within a single tax year. On the surface, this sounds like a win, more flexibility, more choice, more ways to manage your money.

But in reality, it can quickly create unnecessary complexity.

Every new ISA means another account to manage, another login to remember, and another place your money is sitting. Over time, this makes it harder to track your investments and adds friction to something that should be simple.

It’s also important to remember how the allowance actually works. You still only get £20,000 per year in total, and that limit is shared across all your ISAs. Opening multiple accounts doesn’t increase the amount you can invest, it just spreads things out.

From April 2027, there will also be a specific change to Cash ISAs. For those under 65, the amount you can put into a Cash ISA will be capped at £12,000 per year, while those aged 65 and over will retain the full £20,000 limit. The overall ISA allowance remains the same, but with tighter rules on how much can be held in cash.

In other words, the system is becoming more structured, not less. Trying to juggle multiple accounts across providers is only likely to become more of a hassle.

In most cases, you don’t need a new ISA at all. If you’re happy with your provider, you can simply keep topping up the same account and keep everything in one place.

And if you do want to try a different platform, you don’t need to start from scratch. You can transfer your ISA across without losing your tax benefits, and in many cases, providers will even offer incentives to move.

I once went down the route of opening a new platform almost every year. It felt like I was optimising at the time, but it quickly became a hassle, scattered accounts, more admin, and no real benefit.

The goal isn’t to collect ISAs. The goal is to build wealth in a simple, consistent, and structured way.

Pension News

So, what's been happening in the world of pensions?… apart from the usual stuff you see around April… State Pension gets its triple lock increase and your annual SIPP Allowance resets back up to £60k.

Excitingly enough we've got two updates from Parliament.

The Finance Act 2026 has been given Royal Assent, basically becoming an Act of Parliament. What was it about this Bill that's relevant to Pensions? Well, it's now official that from April 2027, unused pension pots will form part of the estate for Inheritance Tax purposes.

Do you benefit from Salary Sacrifice and contribute to your pension that way? Well, lucky you and good for you… for now. You may recall in the 2025 Autumn Budget, the Chancellor signalled the intention to place a cap of £2,000/year on how much employees could contribute to their pension whilst benefiting from Salary Sacrifice. The bill went for a reading in the House of Lords as part of the ping-pong, and the Lords inserted an amendment to increase the cap to £5,000/year and for basic rate taxpayers to be exempt from such a cap altogether. Sadly, the Commons rejected it.

Commons 1 - Lords Nil.

Still, 2 more hearings to go, so write to your MPs.

We still, however, maintain that SIPPs and Workplace Pensions remain some of the most tax-efficient methods to save for retirement, so keep plugging away.

Nisba Insights:

When the smartest people in finance nearly broke the system

In the late 1990s, a hedge fund called Long-Term Capital Management (LTCM) was launched by some of the most respected minds in finance. This wasn’t a typical fund. It included Nobel Prize winners and traders with decades of experience, all working together to build what they believed was a near-perfect investing machine.

Their approach was based on finding small pricing differences in markets and betting that those differences would eventually correct. On its own, that doesn’t sound particularly risky. But to make meaningful returns, they used large amounts of borrowed money. This allowed them to place huge bets on positions that, in theory, were “low risk.”

For a while, it worked incredibly well. The fund generated strong returns and quickly built a reputation as one of the most sophisticated operations in the world. Then 1998 happened.

Following the Russian debt default, global markets became unstable. Relationships between assets that had held for years suddenly broke down. Prices moved in unexpected ways, and the models LTCM relied on could not keep up. What they thought were small, temporary mispricings kept getting worse.

Because they were so heavily leveraged, the losses escalated rapidly. Within a short period of time, LTCM was facing collapse. The problem wasn’t just the fund itself, but the size of its positions. If it failed suddenly, it could have caused a chain reaction across the global financial system.

In the end, the US Federal Reserve had to step in and organise a bailout involving major banks to prevent wider damage.

The lesson here is not just about one fund. It’s a reminder that no amount of intelligence or mathematical modelling can fully control risk. Markets are driven by human behaviour, uncertainty, and events that cannot always be predicted.

From an Islamic perspective, this story is even more relevant. LTCM’s strategy relied heavily on leverage, complex structures, and a level of uncertainty that goes beyond what would be considered acceptable. Islam encourages clarity, fairness, and a real connection between investment and underlying assets, not layers of complexity built on borrowed money.

It also reinforces a deeper principle: wealth should not be pursued through excessive risk-taking or systems that can cause harm to the wider economy. The pursuit of returns should always be balanced with responsibility.

Sometimes, the simplest approach, staying diversified, avoiding unnecessary risk, and investing with discipline, is not just safer, but more aligned with the values we’re trying to uphold.

"This is more halal than that"

This is just my opinion. I’ve been wrong before, many times, and I’ll be wrong again, so take this with that in mind.

There’s a lot of conversation around the “halalness” of Shariah-compliant investments and mortgages. I think these discussions are healthy when they come from a place of genuinely seeking knowledge. Most of us start with limited understanding, so it’s natural to ask questions and explore. Where it becomes more difficult is when people with very little knowledge form very strong opinions.

This isn’t unique to Islamic finance. You see it with debates around halal meat, music, and other areas too. The issue is that these opinions are sometimes built on incorrect or incomplete information, which can lead to confusion and unnecessary division.

My own approach is to be careful about making definitive claims. I don’t position myself as someone who can say whether a product is permissible or not. What I am comfortable saying is that scholars may differ. Some approve certain structures, others don’t.

I may have my own leaning, but it shouldn’t carry weight. While I study Islamic finance and continue to learn, I am not a scholar with deep expertise in the Qur’an, Hadith, and jurisprudence. For that, I rely on those who have dedicated their lives to it.

What I can control is my intention. My intention is to invest in a halal way. I don’t want to earn in a way that is clearly impermissible. And I’m not trying to find loopholes or obscure opinions to justify something questionable. I rely on established Islamic bodies and scholarly groups who assess these matters collectively.

So in my view, you have two options. You either follow the experts, or you become one. InshaAllah, we move closer to becoming the latter.

Final Reflection

After you’ve been investing for a while, something subtle can start to happen. News that impacts people’s lives in a real and serious way slowly turns into a number. The focus becomes not what happened, but what it did to your portfolio. You hear about thousands of people affected, and the immediate reaction becomes “my portfolio is down 3%.” That’s a dangerous shift.

When things start to feel like that, it might be a sign to step back a little. To take a break from constantly checking your investments and reconnect with what’s actually happening in the world.

Most of the time, there’s a loose relationship between the two. When bad things happen, markets often fall. When things stabilise, markets recover. But if we’re not careful, we can begin to associate human suffering with financial outcomes in a way that doesn’t sit right.

It would be a worrying place to get to if we found ourselves even slightly pleased about something harmful happening, simply because it benefited our investments.

That’s my reflection for this week. A reminder to myself before anyone else.

Responses